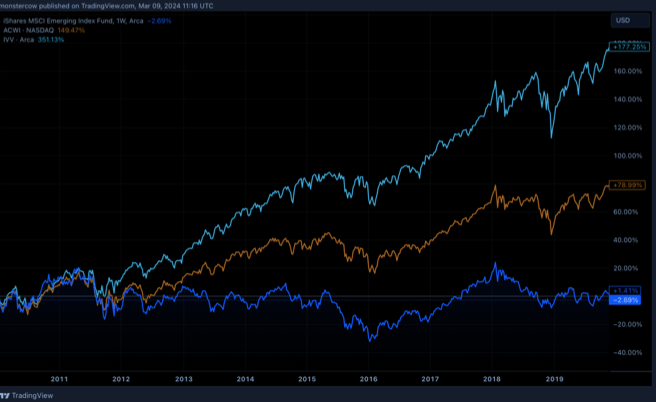

Emerging markets offer investors great returns in exchange of high volatility and undertaking of risk. Let have a look at the past performance of EM , comparing them (orange and dark blue) with the equities market (light blue line).

An index approach towards the EM sector has grossly underperformed the US equities market. If investors are looking for decent returns in the world of equities and cannot afford the luxury of time of research, indexing the NASDAQ or S&P500 will suffice; not ludicrous returns but decent.

So what is the edge, if there is any, in dipping your toes into equities outside of the dominant US market? First we would need to understand why US equities tend to be above par.

USA

The US has everything and anything that an aspiring entrepreneur would want. It offers many ways to capital access, facilitates a conducive regulatory environment and rewards those who dare try to innovate and take risk. This environment has reaped much benefits for those who remained fervent in its cause. Every now and then one can find companies disclosing consistent earnings growth, doing strategic buybacks and providing competitive dividend yields. All these are signs of a robust and rewarding economy, which undoubtedly translates to impressive returns.

Having understand these factors for success allows us to compare and assess the investment environment in emerging markets.

What Matters

Emerging markets typically are markets where their countries are transforming their economies from the Old to New. There is a lot of upside to these markets, as we have seen from past case studies. Take a nation close to our heart: Singapore. From a dilapidated fishing village in the early 1960s to a financial hub now, anyone who has capitalise on us would have seen exponential earnings per share growth.

However, correlating a country’s ability to realise consistent and high GDP growth to investment returns is arguably myopic. It is necessary to understanding the dynamics of individual stock markets, especially where capital inflows are being allocated within the economy. With an added layer of complication of a company’s dispersed area of operations, it makes the process of finding your 10x/100x baggers arduous.

We are witnessing weaknesses in the vibrant US economy, as well as fundamental shifts in the balance of power. EMs therefore remain at an attractive valuation from a historical perspective, and part of a long term diversification amid US structural weakness. Hence, taking a shot in such markets may serve as a palatable alternative investment for some.

The next section are overviews of different economies that we also are keeping a keen eye on.

India

With its amazing demographics, India boasts the world’s largest general and youth populations, and with increasing educated and literacy levels. As India gears up for an election cycle, the Modi government is likely to roll out new initiatives aimed at bolstering the lower-income groups. The BJP party has secured victories in primary polls, boding well in terms of political stability and continuity of policy enactment longer term. The culmination of market friendly policies, strong foreign direct investment inflows in recent years, demographic resilience, India presents a strong structural opportunity in the long term.

Indonesia

Similar to India, their promising demographics offers a springboard for further growth. Indonesia will continue to grow at a strong rate, and possibly becoming the dominant force within SEA. This will likely continue after a relatively stable and smooth election cycle. Under the new President, financials and consumer goods, as heavily domestically oriented sectors, will continue to outperform.

Brazil

Brazil is another macro opportunity that is widely mentioned, as one of the most attractive opportunities. Brazilian equities grew at almost 24% in Dollar terms in 2023, and a strengthening currency, undervalued equity markets (7.5x to the benchmark’s 19). In addition, the market also pays a 7% dividend yield. Its consistently declining unemployment rate has allowed the Central Bank of Brazil to make consecutive rate cuts.

Mexico

Mexico stands to benefit from the reshuffling in global supply chains. Demand remains afloat with strong real wage growth, increasing government spending ahead of elections, growing remittances and a strong FX with a positive real rate. Growing nearshoring opportunities should provide continued tailwinds, and has driven a 28.6% y.o.y growth in fixed capital investment to reach the highest on record. Inflation has fell, while rates remain elevated historically. The possibility of lower rates, stronger consumerism and investments provide possible justification for Mexican equities to continue growing.

Leave a comment