I have always enjoyed a good read. Hence it wasn’t much of a surpise that when Wall Street delivered their Annual Shareholder letters, I found myself immersed quickly in the thoughts the best had to offer.

Of the many insightful pieces, BlackRock’s Laurence Fink stood out to me the most for his unbiased, market oriented and calming tones. It provided a breath of fresh air amidst a sea of noise and fear-mongering that makes investors question our decisions day in day out.

In his letter, he outlines how his parents who were unassuming humble workers managed to generate a disproportionately large nest egg through the power of staying invested and making wise financial decisions. He opines that the growth and prosperity of the capital markets will remain a dominant economic trend through the rest of the 21st century.

In my view, the America of today and the one his parents accumulated wealth from is structurally worlds apart. America today is a tale of divisive people, no longer bound together by faith in the flag but by an inability to reconcile on clear differences and bipartisanship largely all but a fantasy.

In this article, we’ll take a look at some of his insights, as well as my view on the state of the American story.

I see 5 fundamental national security threats that could derail an American-lead world order:

1. Fiscal Debt and De-Dollarization

2. Polarisation in America

3. Disinformation and Distrust in Institutions

4. Breakdown of Democracy

5. Geopolitical Fragmentation

Let us take a closer look on them:

Debt

US debt in just the past 20-25 years has grown a staggering 600%. As debt continues to outpace their economic growth on top of foreign government’s waning purchase of US debt, I see potential in a worst-case scenario of a period of austerity and stagflation. Forced austerity could severely hamper the conducive environment for innovation and investment that they have managed to cultivate over the years, similar to the way Europe suffered in the aftermath of the Great Financial Crisis. In another vein, the US likely does not have much bandwidth to take up drastic austerity measures due to the largely non-discretional nature of their spending.

Additionally as US continues to grow their debt unsustainably (adding $1 trillion in debt every 100 days according to BofA analysts!), the attractiveness of the perceived ‘risk-free’ Treasuries will start to wane. In 2023, Fitch downgraded US fixed income holdings and Moody’s lowered US debt ratings to a ‘negative’ in response to the fiscal deficit. For the US to continue to sustain levels of borrowing and spending, it will have to raise bond yields to attract more buyers, further eroding the trust in the US debt. Settling at a higher borrowing rate also results in businesses and individuals to suffer greatly.

Laurence Fink believes that a public-private partnership for credit has to be the way forward. I see a debt and payments restructuring to be complicated but necessary, while the partnership to be vital in key areas such as innovation but not essential services. Take the Inflation Reduction Act for example; some funding could come out from partnerships with EV makers for charging infrastructure instead of being wholly funded by the government. But areas such as healthcare should be prevented from becoming privatised as much as possible.

Of greater concern is the shift from rate-sensitive to rate-insensitive bond buyers. We’ll touch on that in another Perspective.

Polarisation

Since the 1990s, political polarization has increased in the US with voters and investors seeing the 2 parties as offering increasingly divergent platforms.

With each camp of ideology perpetuating biases, it creates brain fog that greatly skews decision-making of people, even those employed to make the tough ones. Increased polarisation and the inability to reach bipartisan agreements on an increasing multitude of issues adds to American incompetency in governance and slows down bureaucratic processes, fuelling uncertainty in the macroeconomic environment and deterring investment.

As a whole, passing of public laws that benefit the economy and welfare become less likely and the anti-cooperation in extreme cases, allows the country to make extremely controversial decisions such as the overturning of Roe v. Wade and allowing of states to censor education.

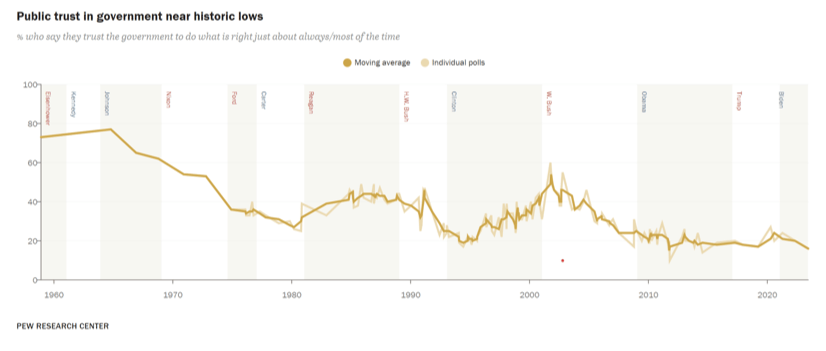

Distrust

Instead of solving sensitive issues, there is a proliferation of disinformation and misinformation that sows the seeds of distrust. What we are seeing now is the pinnacle (or nearing it) of a “They vs Us” narrative.

The rise in AI integration especially in deepfakes, hallucinations and the potential to destabilize has also come at the worst possible time when we are barely able to cope with the prevalence of disinformation. This should be a key global risk in the coming decades considering disinformation is being produced easily and with unparalleled realism and scale of dissemination. As Cambridge notes, although disinformation is a long-standing issue, AI aggravates the issue by allowing effective manipulation at large scales and direct amplifies the spread of such content, considering AI systems are programmed to enhance engagement.

Along with the rise in polarisation, populist sentiments and policies by divisive candidates are gain popularity, perpetuating problematic beliefs that are not beneficial for the US in the long run. As a country, policymaking begins to corrupt from within.

Ultimately, disinformation and distrust are of utmost threat to American stability. Confidence and trust are essential to legitimacy and the ability of institutions to operate effectively and smoothly. It also goes without saying when policy missteps are noticed, it adversely affects public trust.

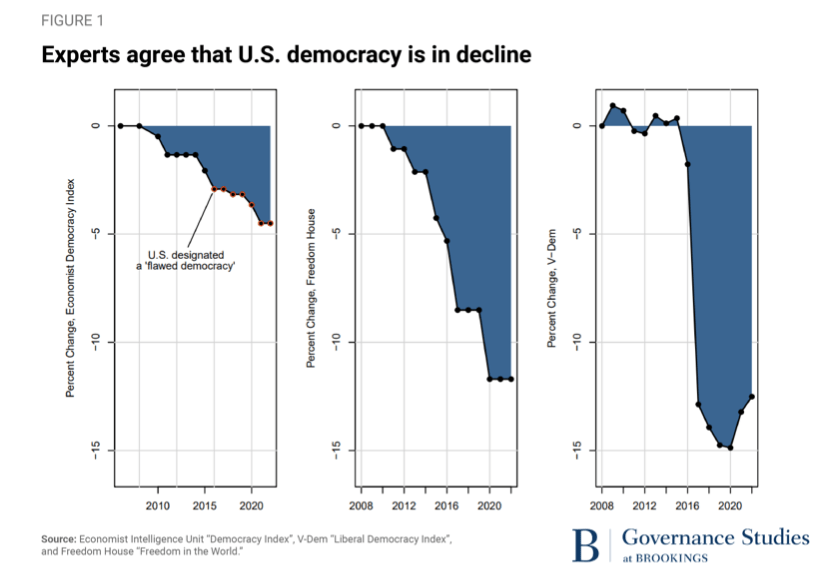

Breakdown of Democracy

3 years later, there is still no definitive resolution to prevent the catastrophe of Jan 6 from happening again. In fact, it looks likelier than ever. The events on Jan 6 were one of the most blatant threats to democracy in American history where polarisation had reached such a level where parties were willing to take up arms and overthrow the government.

This is a culmination of the aforementioned 2 points. With America constantly hailed as a bastion for freedom and democracy, such breakdowns of proper dialogue and decorum are unacceptable and detrimental for the global economy. Moreover, its appeal as a global investment destination due to the stable financial markets and predictable environment would be undermined in the event of any significant democratic processes.

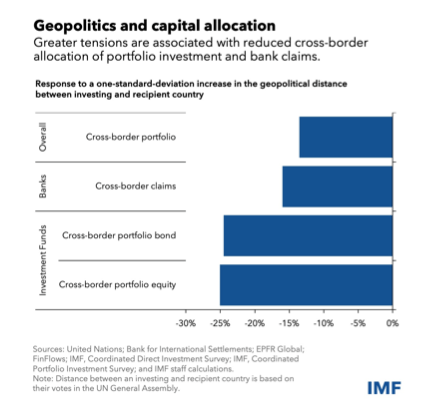

Geographical Fragmentation

Global relations and international tensions are at their worst since the Cold War. In the world now marred by West-BRICS hostility and more countries looking to shore up alliances with BRICS, American dominance might be in more of a threat than the Cold War, where China’s open market policy led to stronger cooperation between China and the US.

According to the IMF, long term costs of trade fragmentation alone could range from 0.2% of global output in a limited fragmentation scenario to 7% in a severe scenario, roughly equivalent to the combined annual output of Germany and Japan. If technological decoupling is added to the mix (which we are seeing right now), countries may see a loss of up to 12% of GDP. IMF analysis show that the full impact would be even larger when factoring in restrictions on cross-border migration, capital flows and decline in international cooperation that would leave us unable to address the challenges of a shock-prone world.

Longer term, greater financial fragmentation derived from geopolitical hostility affects cross-border capital flows and intensifies risk by limiting international risk diversification. This puts the global economy at a more vulnerable spot than it already is, especially if the global financial safety net breaks down.

What We’re Saying

The point of this article is not to sway anyone’s beliefs or to tell you NOT to be invested in the American markets. That could be further from the truth. Even if America were to implode, it’s highly unlikely it happens in the next decade or two.

The complex thing is that it is not as simple as simply divesting from the American markets for alternative markets instead even if you do believe the American miracle would be ending soon. Despite the challenges America faces, it still boasts:

- The most conducive environment for enterprise, startup and innovation;

- The most favourable environment for business;

- The most secure financial and capital markets in the world due to the strong and established regulations, robust frameworks and capable financial governing authorities;

- The global reserve currency , and enjoys a lack of strong alternatives unless BRICS launches a collective currency. That seems unlikely, since Russia is pushing forward their CBDC Ruble, China wants the use of the Yuan to proliferate and the presence of tensions internally;

- The strongest and most reliable capital markets in the world, with the highest liquidity and provides a relatively safe investment avenue for international and institutional investors. The American capital markets are held up by some of the strongest financial institutions, each with trillion in assets, to ensure the capital markets do not collapse;

- The strongest economy in the world, backed by the strongest capital market in the world, allowing it to recover from economic downturns quicker.

I’d like to focus on one more thing that stood out to me in Laurence Fink’s letter:

“After all, investment (or lack thereof) is just a measure of fear because no one lets their money sit in a stock or a bond for 30 or 40 years if they’re afraid the future is going to be worse than the present. That’s when they put their money in a bank. Or underneath the mattress.”

This observation is especially apt in contextualising investors’ fears of the future of the American economy. The current state of the macroeconomy drives some long term structural questions that we look far from getting a response on. But should an investor looking for growth opportunities, but wary of the path the American economy is going to undertake, look towards alternative markets?

Leave a comment