I’ve explored the current trends that are worrying, and clearly established that the America of today faces some very daunting and unprecedented threats. There are many investors who feel the same and have been looking for alternative markets to diversify risk.

Conventionally, retail investors flock to the next big growth story (eg. China, India) because of media attention and projections of strong economic growth in those regions. But their decisions can at times be largely unfounded on assumptions that strong economic growth correlates with proportional equity market returns. But is this the case?

In 2002, authors Dimson, Marsh and Staunton documented a surprising pattern: there was a negative correlation between per capita economic growth in a country and that country’s stock returns from 1900 – 2000, with both variables adjusted for inflation. Subsequent research by these authors expanded the number of countries and added data through 2019 and a negative correlation, although not quantitatively significant, continues to exist.

Today, we hear lots of mentions of the next global superpower. India has been in contention for years and that holds some truth.

Bloomberg Economics has India’s economy on track to overtake China’s as the world’s biggest growth driver by 2028. India boasts a young, robust and talented workforce with labor participation set to increase well into the century, while its dynamic business environment attracts many MNCs looking to divest operations from the more uncertain China. Apple opened its first retail stores in India last year, and the iPhone 15 became the first generation to launch units made in India as well as China. Tesla is reportedly ready to invest up to USD 2 billion to set up an electric vehicle factory there.

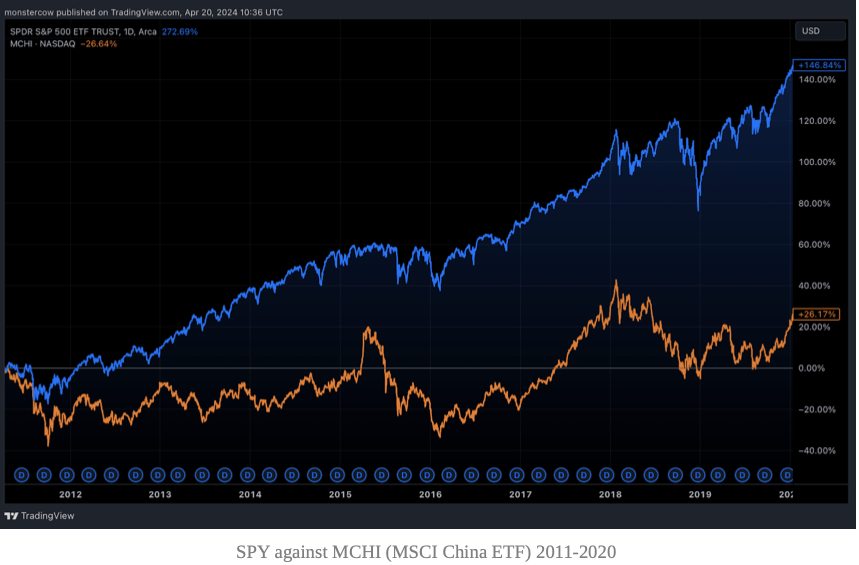

If we dial back our focus on the previous golden child, we notice that since the 2000s investors have been lured by the growth projections of the Chinese economy. By the end of Q1 2011, the combined market capitalisation of China’s Shanghai and Shenzhen stock exchanges exceeded USD 4.2 trillion, a significant rise compared to USD 400 billion in July 2005. The introduction of stock index futures access in April 2010 was also met with high levels of interest from retail investors.

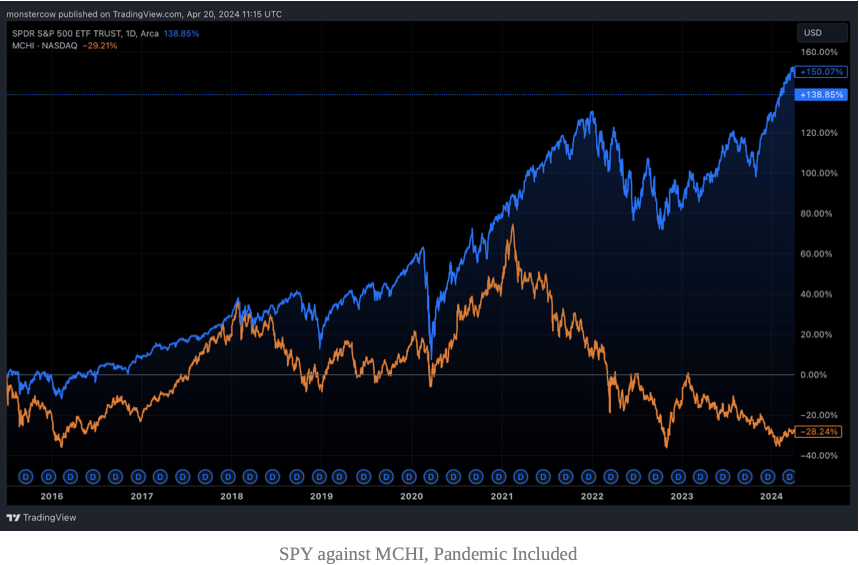

In spite of the much stronger economic growth, US equity markets have vastly outperformed the Chinese equity markets. Refer to the charts below to understand the extent of dispersions in equity market returns.

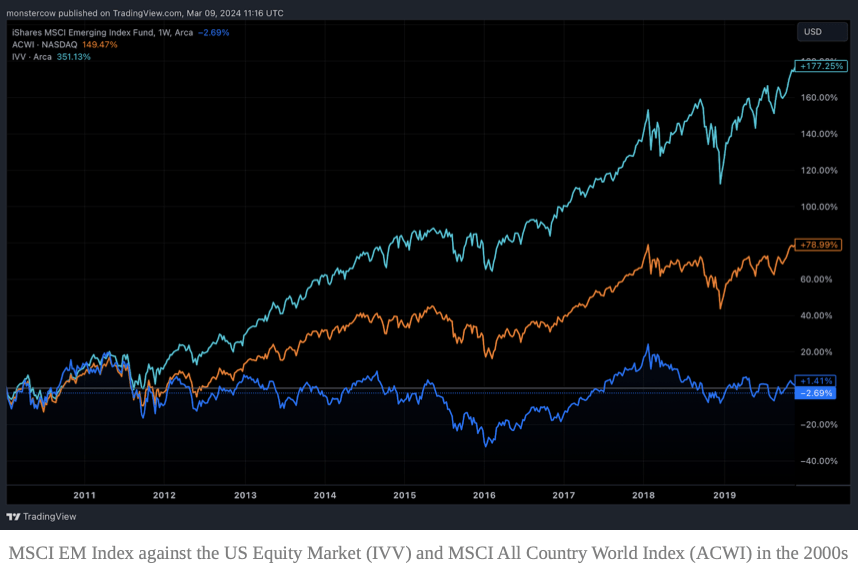

US equity outperformance is not limited to the Chinese equity markets. Since the Great Recession, the S&P has tactically outperformed global equities consistently. If we were to look at the past decade, the US S&P exponentially outperformed the Emerging Markets (EM) index as well as global equity benchmarks (ACWI). Note that the ACWI is largely overweight US equities still.

In the study referenced earlier, Dimson, Marsh and Staunton proved that GDP as a growth driver is not as indicative as EPS growth. A company that grows its earnings but issues an equivalent number of new shares will see its market cap increase, but not the per share price. At the country level this is similar. If a growing country sees an increase in number of companies going public but they do not become larger, the country’s economic numbers grow even if it means the current companies do not. In essence, what drives GDP growth are factors such as increased capital, labor, improved technology and efficiency driving higher output, but these increases in factor accumulation and productive technologies have mainly benefitted consumers rather than owners of capital.

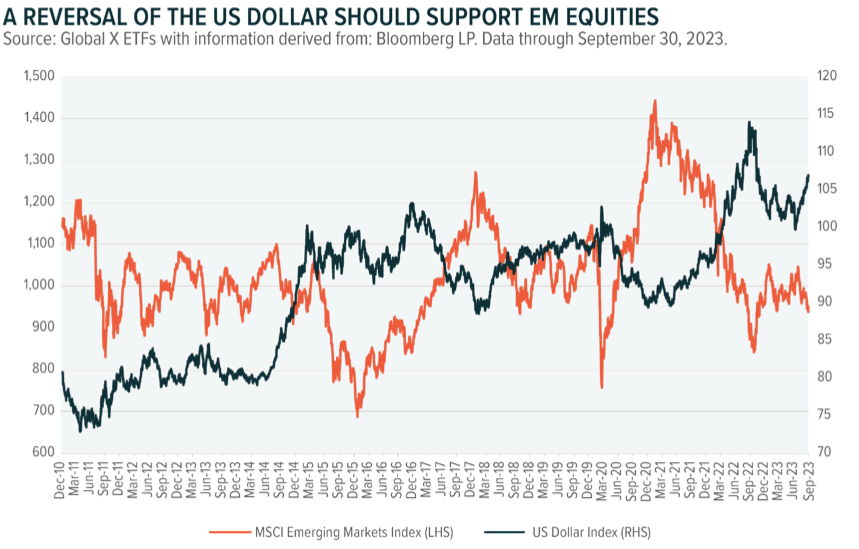

The considerations when looking at alternative markets increase exponentially as well, as compared to the US markets. One of these principle considerations are strengths of domestic currencies.

- International equities have displayed inverse relationship with the Dollar

- Unlike the Dollar where investors can stay relatively assured of its stability, international currencies display higher volatilities, partly because many major commodities are denominated in Dollars

An example of these considerations in play is in the 2024 outlook. Many investors and institutions expected a Fed pivot to benefit international equity markets, particularly EM equities. Historically, EM equities have gained roughly 4% for every 15 downward move of the Dollar. However, with inflation proving to be stickier than ever and the Fed showing no signs of expediting the rate cutting process, Dollar yields have strengthened, leading to a stronger Dollar and depreciating international currencies. Of course, this negatively impacts alternative market equity returns.

Geopolitical risk still remains one of the key macro themes through the 21st century and hedging that risk can prove rewarding for value investors as well as tactical portfolio managers. That said, I dissuade those who look at countries with lucrative growth forecasts and assume capital market returns will be of similar scale. There is no benefit if those countries themselves, do not have strong domestic capital markets and residents do not have the propensity to invest their growing affluence savings into their own markets. But opportunities do arise when investors go granular:

- Indonesia will continue their trend of strong growth, with an evolving macro landscape and a relatively smooth transition of power. Financial and consumer goods as heavily domestically oriented sectors will continue to outperform

- Brazil is one of the most eye-turning opportunities in 2024, spurred by strong equity returns in 2023 (24% in Dollar terms) and a strengthening currency. The market also pays a 7% dividend yield, making it an attractive opportunity for dividend investors. Longer term, it boasts a declining unemployment rate, which has allowed the Central Bank of Brazil to make earlier rate cuts than most of the developed world

- Mexico and Vietnam will blossom as connector countries due to the heightened geopolitical tensions and restructuring of supply chains. Nearshoring has provided strong tailwinds for Mexico, driving a 28.6% YoY growth in fixed capital investment. Considerations are a lack of fiscal prudency (and associated high debt levels) and strong dependence on external markets economic performance

I mentioned much about alternate markets in general, and how investing in them might not be as straightforward as we take the American equity markets to be. This is because of some comparative advantages that made the US stock markets the most lucrative in the world, and the largest by far.

And in spite of what I have listed in the previous article, I feel it is only right to manage this fear. We have to acknowledge that the USA capital markets are far more robust and resilient than we tend to give credit to.

In Laurence Fink’s letter, he talks about the strength of US capital markets that allowed the economy to rebound much faster and stronger than its international counterparts. As a strong source of secondary funding, the US capital markets drive innovation and business growth, perpetuating a self-fulfilling cycle of growth and capital market expansion.

US capital markets are also supported by world-leading capital market infrastructures (CMI). With a comprehensive network of organisations that manage execution, clearing and transaction settlements, investors enjoy efficient trade execution, reliable post-trade services and secure custody of assets.

The US capital markets’ integration with global capital markets allow them to attract and retain global investment in an unparalleled fashion despite geopolitical tensions that could have affected capital inflows from regions. The resilient supply of foreign capital investment enables continuous funding and liquidity for American firms, allowing them to continuously innovate and grow. This in part arises from their status as the world’s reserve currency. Since the post-WWII era, the preeminent role of the US dollar in the economy has provided an unmatched depth and liquidity of financial markets and as of 2021, the dollar comprised 60% of globally disclosed official foreign reserves.

The main takeaway is that one should not haste to completely discount the US capital markets just because of its waning geopolitical climate and unwelcoming economic environment. Additionally, alternative investments to those in the US that are on par or superior in delivering US’ returns are far and few.

As we navigate new global uncertainties and reflect on recent developments in global influence, we note that the landscape of American dominance is changing but not necessarily eroding. Throughout history there were plenty of reasons to be divested, but those who stayed the course saw immense wealth accumulation.

Careful to avoid making the same mistake, we view present challenges as opportunities to adapt strategies and our roles in the global arena. While the US faces structural headwinds, we have learned that strength does not have to solely depend on the fortunes of one nation.

Leave a comment