(15 minute informative read)

Singaporeans are well aware of the meteoric rise it has had to the top of the financial world. The growth story behind Singapore’s financial sector was far from a miracle though. In the 80s, recognising the need to diversify from maritime trade, Singaporean leaders identified the financial sector as a key area for growth following a significant recession. The strategic foresight displayed has since saw Singapore’s transformation into a diversified and resilient economy, with maritime trade making up only 7% of GDP.

Not along ago, I chanced upon mention of a GFCI report, detailing how Singapore has on key indicators became a world-leading financial centre.

For those that are unfamiliar, the Global Financial Centres Index tracks 5 key pillars of a financial centre: Human Capital, Business Environment, Reputation, Financial Sector Development and Infrasture. In true Singaporean fashion, it does exceptionally well on structured scorings ranking just behind New York and London. But Singapore just doesn’t feel like it has the same draw and pedigree as the other top financial centres it ranks on par with – at least not to me.

A huge factor for my consideration is the state of our capital markets. I hold a firm belief that Singapore cannot truly be a top financial hub unless it develops a respectable capital market. Macroeconomically, the presence of a strong capital market is paramount for providing a reliable secondary market for funding and more importantly greater international involvement in Singapore. At the surface level, our deal volumes and valuations will always remain suppressed as long as we do not have a competitive equity market. In fact, Singapore has one of the lowest equity market activity in the world. Without building a competitive and attractive global capital market, how is Singapore supposed to be mentioned with the likes of Hong Kong, London and New York?

For the purpose of making this digestable, I will focus on just the equity market. But this doesn’t discount the significance of a robust bond market and its deep liquidity in supporting strong economic growth and fostering a vibrant business environment. I’ll get to that another time.

Why is the SGX important?

Like I mentioned, it is challenging for Singapore to have international allure it should have with a weak and stagnant stock exchange. A strong equity market is paramount to

- Drive up deals and valuations, attracting bankers and financial activity

- Provide a reliable secondary market for funding. As a small and open economy, Singapore is incredibly vulnerable to exogenous shocks. Fortified by resilient source of credit, economic agents will be more resilient to financial risks. This is all the more relevant to domestic businesses

- Increase economic resiliency through derivative instruments and financial products, allowing businesses to hedge against market volatility and currency risks

- Further drive growth by providing much-needed capital for productive investment and financing corporate growth. This is pivotal in supporting industrialisation and technological innovation without putting fiscal strain by relying on government funding

The last point is significant. The Prime Minister Lawrence Wong, just mentioned that Singapore ‘cannot afford to outbid the big boys’, referring to how larger countries have greater ability to spend more on subsidies and building up capabilities in strategic industries. Much like in South Korea or China where capital markets have supported productive investment, Singapore by enabling domestic firms greater access to alternative sources of liquid funding, will be able to make up for its small domestic market with a larger international capital market inflow. This will play out as a crucial step in maintaining Singapore’s competitiveness in the global arena.

Lawrence Fink, the Chief Executive Officer of BlackRock, the world’s largest asset management aptly notes the importance of the capital market in his 2024 annual shareholder letter:

“Why did the US rebound from 2008 faster than almost any other developed nation? A big part of the answer is the country’s capital markets…. Countries aiming for prosperity don’t just need strong banking systems – they also need strong capital markets”

To truly become a key gateway between Southeast Asia and the rest of the world, Singapore has to work towards attracting regional firms to list on the SGX. Singapore has the ideal conditions to make this a reality and should actively be working towards this goal because it has these key pillars in place:

- A world-class legal and regulatory system governed by the Rule of Law, fundamental to the development of a strong and stable business environment

- Strong diplomatic and business relations with most of the world, providing regional firms the perfect opportunity to gain outreach and connectivity (I see this playing out similar to the rationale why chinese firms choose to Singapore-wash their operations)

- A strong and steady wealth inflow – the number of millionaires in the island-city just rose to more than 333,000 in 2023 whilst the global tally shrunk. We already have huge draw for foreign wealth vehicles due to our capital and tax friendly laws. Singapore needs to leverage on the vast wealth parked onshore

- A potential shift in influence away from Hong Kong and Taiwan, as international investors increasingly factor geopolitical risks into their portfolio allocations and such risks form key macro trends that will continue for the rest of the century

- Compared to regional peers, Singapore enjoys a strong and stable currency as the most developed market, providing reassurances to regional firms that choose to list on the SGX

Role of the SGX

Different capital markets around the world provide different value; while Saudi Arabia builds up a market for mortgage securitisation, Japan and India focus on a savings market, the SGX has served as a conservative dividend paying market for domestic investors.

This plays in part to the underperfomance of the Straits Times Index compared to international counterparts. Conventionally, dividend payers are less likely to generate sizeable returns because surpluses are returned back to investors instead of reinvested to further grow profitability and revenues. Yet perhaps this is what Singaporeans prefer, with Asians generally being more risk-off people and reflected in their businesses and investing habits. Japan struggled through the lost decade and failed to generate significant returns whilst companies boasted exceptionally robust balance sheets and locals focused more on savings than investing. Americans in contrast actively seek opportunities to re-enter the market after downturns and Asians generally became more risk averse after the Asian Financial Crisis. Risk befits rewards, the American propensity to leverage up and take more risks compared to their international counterparts has allowed them to become far and above competitors in valuations, creating a vibrant equity market that attracts international companies who seek higher valuations and funding.

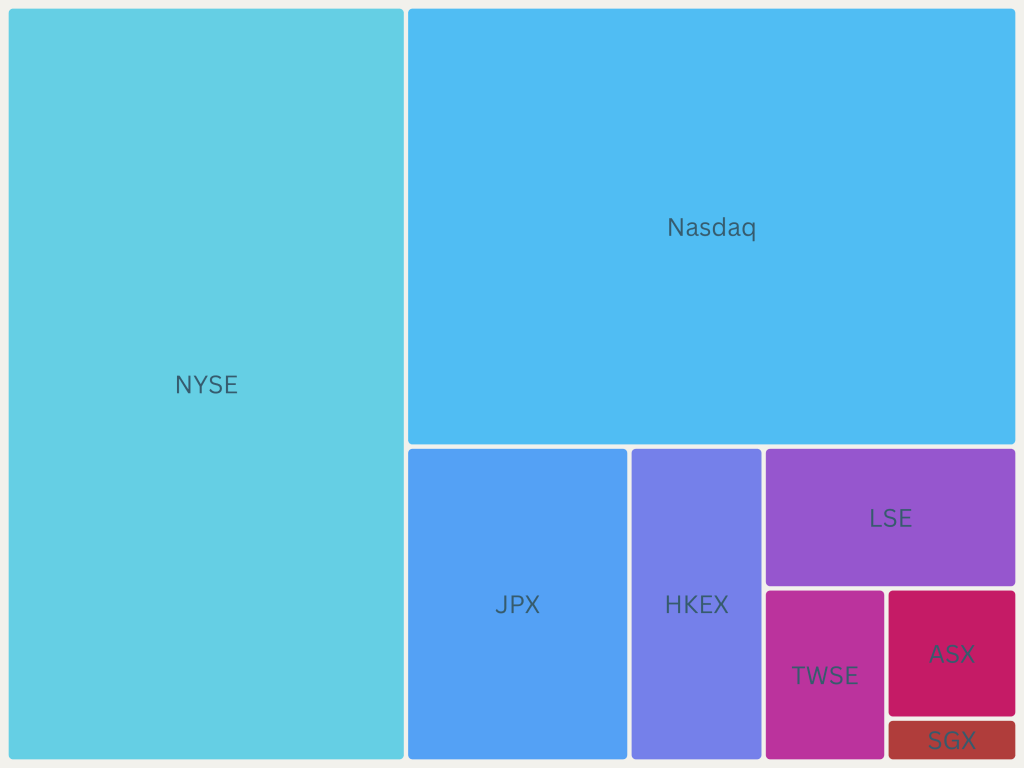

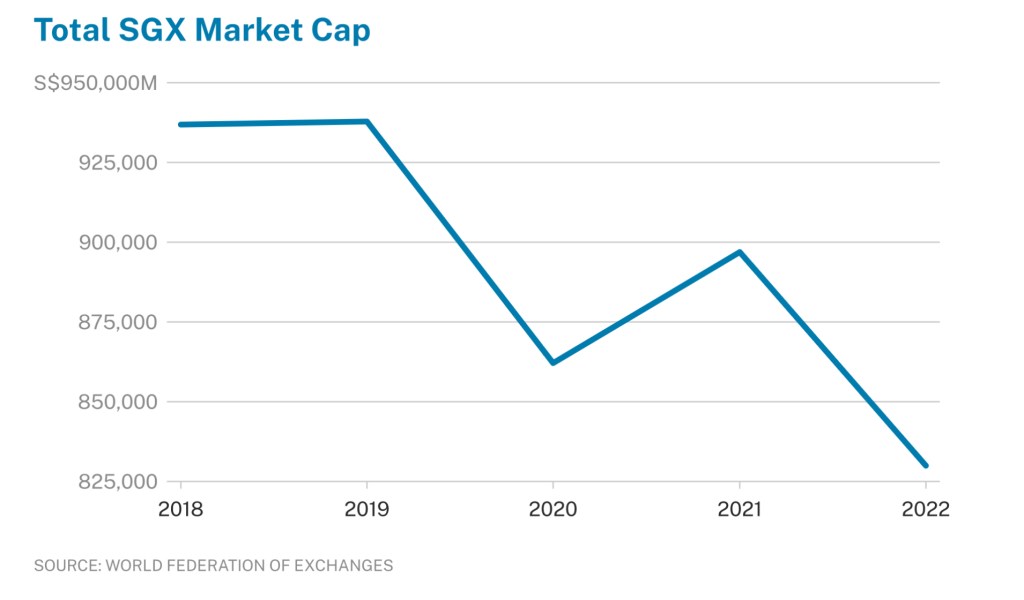

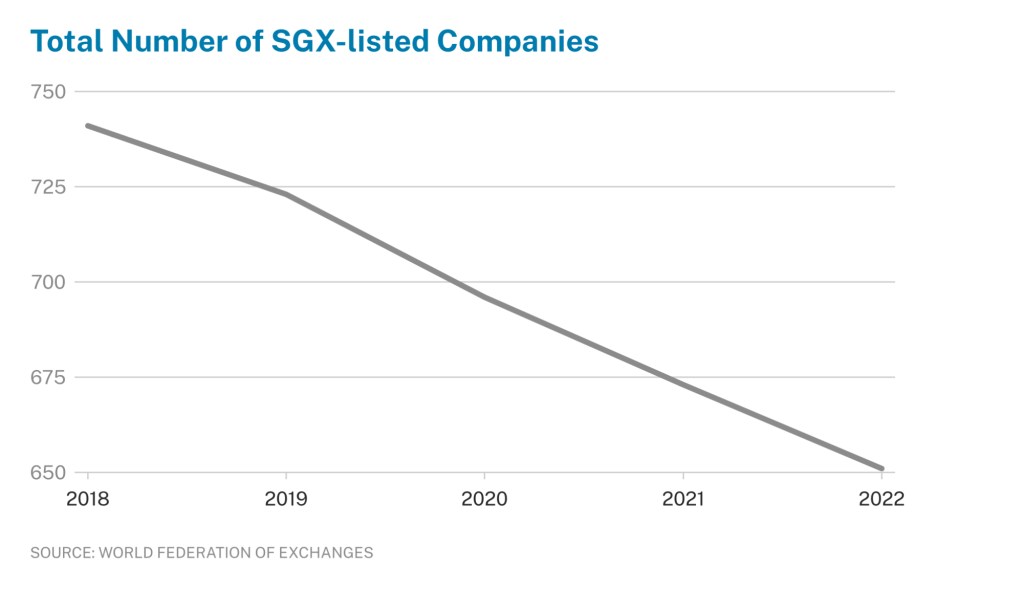

State of the SGX

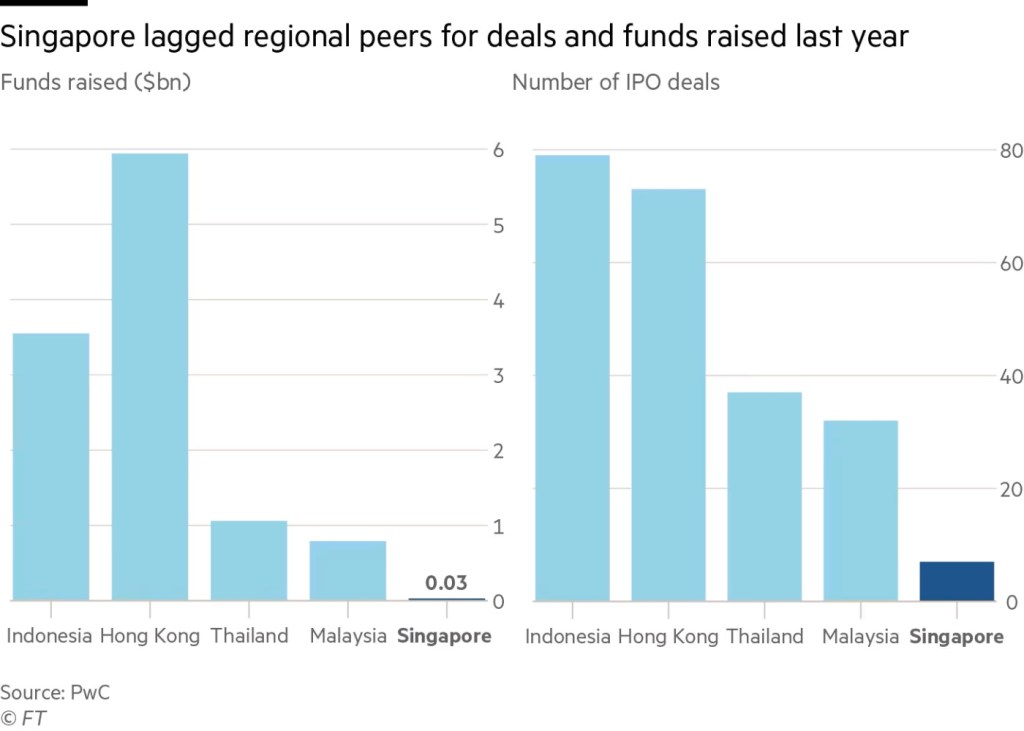

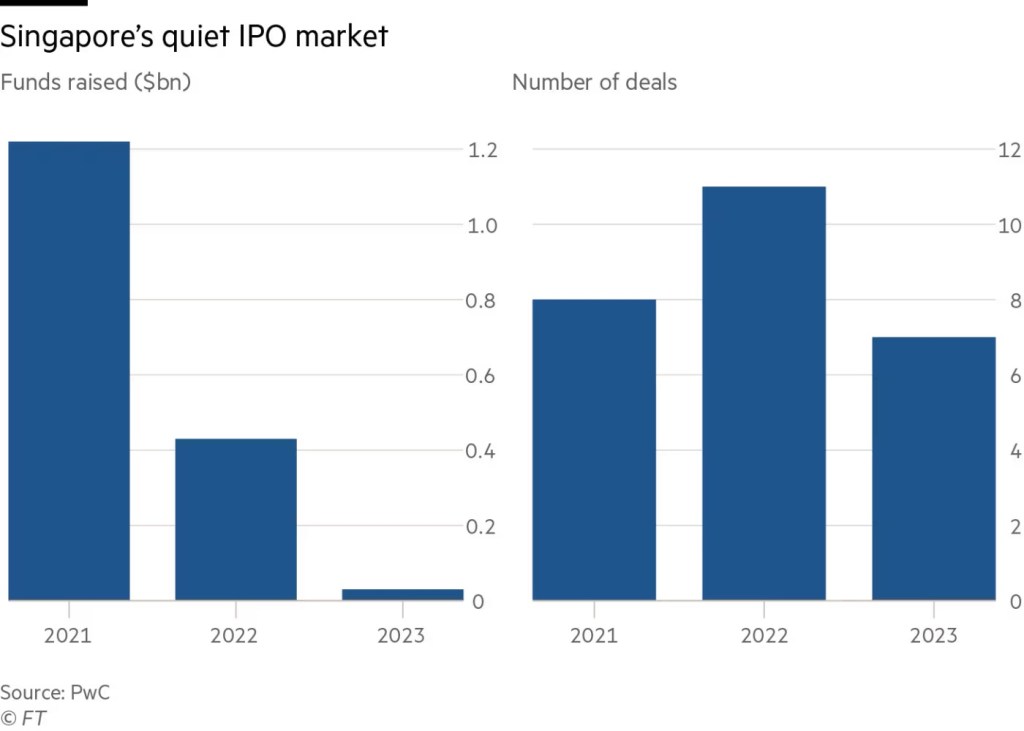

The Singapore Exchange (SGX) has seen better days. Back in 1993 a stock market boom, fueled by strong retail participation and the listing of prominent companies such as Singtel led to a staggering 60% growth in investor returns and many dreamt about becoming a broker. Today the SGX is but a shadow of its past glory, suffering from low liquidity, poor valuations and an unexciting market with only a meagre one IPO in H1 2024 (and at a small scale: SAM Holdings which raised USD 20mm was the smallest in the region!). Through 2023, the SGX only drew 6 IPOs and raised USD 35mm, a staggering 92% decline YoY. This isn’t just reflective of poorer macroeconomic conditions – the SGX has been plagued by a persistant outnumbering of delistings over listings. Year to date, we already have over 10 exits.

Competitive firms are choosing to list abroad in more lucrative and liquid markets. We’ve lost automotive marketplace Carro amongst other notable names such as Grab and Ryde. The issue is they are absolutely justified in doing so. For all of the heralding Singapore has about being a financial hub, the SGX is one of the quietest globally in terms of deals and funds raised. This creates a self-perpetuating cycle where quality firms, faced with more liquid markets abroad choose not to list on the SGX, further exacerbating the issue of lack of competitiveness of domestically-listed firms, in turn having less attractiveness to investors.

The fall in listing activity and liquidity doesn’t necessarily mean that firms are being starved out of alternative funding. Although the equity market is a well established source of secondary funding, more today are looking out for family offices, venture funds and private equity to raise capital. In the latter, Singapore is an overwhelmingly strong market securing almost half of capital investment for the region and picking up 62 out of the 109 deals done.

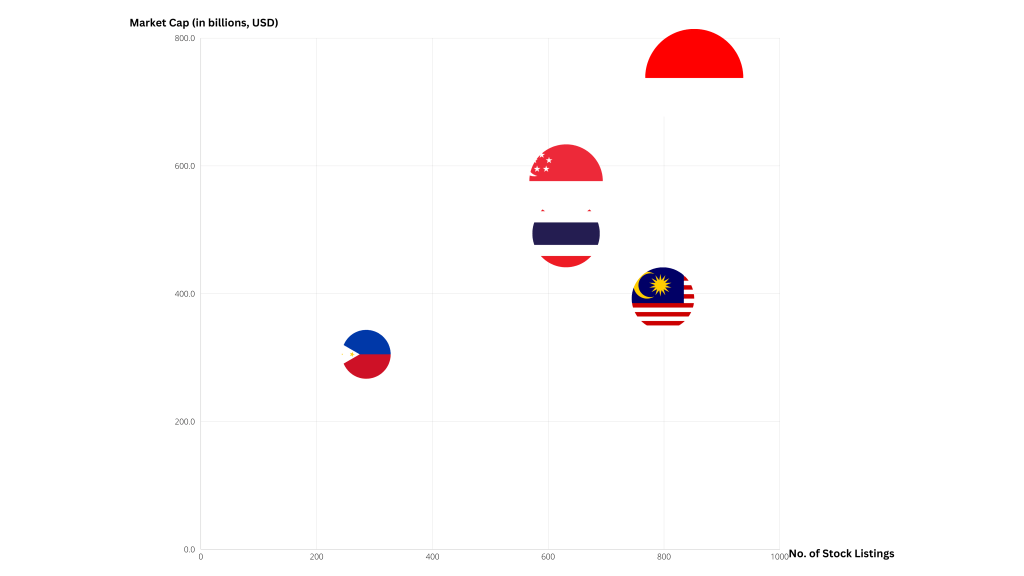

On another note, Singapore markets itself as a gateway to Southeast Asia and a key market player in Asia. Yet in our region, the Indonesian Stock Exchange is among the top 5 exchanges globally by total number of IPOs in 2023 and India recorded its highest number of IPOs since 2017 at 234, an increase of 56% YoY. Under Jokowi who made developing the capital markets a key priority, the IPO market became much more vibrant including highly publicised listings such as GoTo, while market capitalisation has grown by an average of 12% each year. There’s no need to get started on Japan or Korea.

What have others done?

Many countries understand the important tailwinds that a robust set of capital markets bring to economic development and stability. Here are some examples in brief, of what our international counterparts do.

China issues the “Nine-Point Guidelines” to develop capital markets and lays them out every decade. In the most recent iteration, the policy narrative has shifted from “healthy development” to “supervision to prevent risks” and “high quality development”. The measures call for improved IPO listing rules, strengthening information disclosure, deepening reforms on delisting and disposal and promoting five key areas (tech, green investments, inclusivity, pensions and digital infrastructure). Broadly, the focus was shifted towards improving quality of stock offerings, encouraging dividend payments and plugging corporate governance loopholes.

Japan has introduced a comprehensive set of market reforms to tackle issues of corporate governance and incentivise retail involvement.

- The Tokyo Exchange Group requires listed companies to “comply or explain” if they are trading below a P/B ratio of 1, indicating they are not deploying capital efficiently

- Increased accountability to prevent delisting and increasing attractiveness of listed firms

- Focus on boosting shareholder returns and record share buybacks in 2023. Return on Equity (ROE) and P/B ratios have increased following these reforms

- Retail participation grew through the new tax-saving NISA program (Nippon Individual Savings Account). Japanese had higher propensity to save before

- Increased foreign investment inflows, setting new highs in foreign purchases of Japanese equities

- Japan consulted key institutional partners such as Fidelity in the process of drafting out capital reforms

- Whilst the rest of the world prioritise increasing accessibility and reducing red tape, Japan’s reforms are an outlier in the global markets and has aided it in creating a vibrant and healthy economic environment

The United Kingdom has set out changes to how companies list on the London Stock Exchange (LSE).

- The new Labour government plans to reduce red tape and focus on reviving growth and investment to attract innovative companies to list

- Enhanced voting rights and listing pipelines that better support companies to list

- Strong electoral victory provides stability in policy outlook

- Encouraged pension funds to invest more in equity and IPOs to counteract increased foreign outflows. Pension funds currently favour other asset classes over equities, with only 6% of funds allocated to UK equities in 2021

- Reforms were made behind the desire to compete more effectively with Amsterdam, Paris and the rest of Europe

Australia and the US have pensions and retirement savings plans (401k) where money is recycled back into their capital markets. This is translatable to Singapore, only if trust is brought back into the SGX. But by successfully doing so, Australia has kept the ASX liquid and supportive of domestic listings, which in turn attracts international investors

Is Singapore doing anything about it?

The SGX has been studying proposals to improve its performance as the gap between domestic and regional performance widens. Previous efforts such as tie-ups with the Nasdaq and Tel Aviv Exchanges to attract secondary listings, or SPAC regimes being introduced in 2021 have failed to work. The creation of funds to invest in companies as well as schemes to reduce listing costs and reserch coverage also has enjoyed limited improvements, with listing fees making up a small fraction of total costs.

There has been mention about leveraging our sovereign wealth fund GIC to inject liquidity into the SGX. I strongly disagree with this solution considering it compromises GIC’s ability to carry out its mandate of generate attractive real returns and growing Singapore’s reserves responsibly. Investing abroad provides a key diversifier in growing our official foreign reserves and better risk-adjusted returns lie in opportunities abroad. With the extent that Singapore relies on investment returns by our SWFs, the freedom at which they operate should is cardinal.

The recent incorporation of the world’s first APAC financial sector ETF in the SGX might provide some much-needed inflows, especially as international interest in the region grows.

Singapore could perhaps take a stronger position on green finance to increase attractiveness in the region. An estimated $8-10 trillion in annual investment is required for developing countries to achieve the Sustainable Development Goals (SDGs) by 2030. By making green finance a pivotal part of the SGX, Singapore can position our capital markets to be a go-to, reliable source of funding that contributes to regional businesses’ growth and stability.

Moving forward…

Singapore sits in a catch-22 situation: to effectively raise equity market partcipation, it needs its domestic firms to be competitive and robust, but to incentivise these firms to list in Singapore, it needs to raise equity market participation to increase valuations and funding. The focus for the next decade should therefore be on retaining competitive companies as well as building a vibrant startup ecosystem, alongside fostering favourable business conditions for domestic firms to compete. Additionally, ensuring that listing procedures and processes are not overly restrictive goes a long way in flipping the trend of low listings, high delistings. There should also be reforms working in the direction of increasing retail and institutional involvement in the SGX, starting with the allowances for retirement funds (such as raising the limits on investable percentages).

Singapore sits in an enviable position with a clear and workable blueprint to develop perhaps the largest equity market in SEA. As geopolitical uncertainty and public policy shape macro trends and influence investor decisions, Singapore offers a unique blend of reliability and hedging against such systemic risks. With a stable governance and a comprehensively developed regulatory framework, it can leverage on market confidence to build up its equity markets and provide a boost in liquidity. In addition, it already is a premier destination for foreign wealth with favourable tax and business policies, presenting a golden opportunity to develop the capital markets if it is able to spur domestic equity market participation from said foreign capital inflows.

Solidifying Singapore’s position as a leading financial hub requires a concerted effort to develop capital markets with deep liquidity. The benefits are pronounced – they empower domestic businesses with accessible sources of funding and reduce reliance on banking sectors, foster entrepreneurship and provide necessary tailwinds for sustained economic growth. And as a bridge between SEA and the world, the aim should always be after nurturing a robust business ecosystem, to attract regional peers to list on the SGX. Only if Singapore is able to develop this pull, will our ties to the rest of the world as a bridge to Southeast Asia take up more legitimacy.

Arguably, Singapore is already doing well in the financial sector with underdeveloped capital markets. But I strongly believe that now isn’t the time for Singapore to rest on its laurels, or enjoy the harvest after decades of careful and strategic foresight. Singapore has worked its way up from nothing over the past few decades, but the world today poses significant threat to any country much less a small and open one like Singapore. Geopolitical tensions, heightened competition and development of new key markets such as India mean Singapore’s position as a significant player can be overturned as easily as it was built. The pursuit of further developments such as in the capital markets is hence not a luxury, but a vital opportunity that Singapore has to aggressively grab while it has all the stars aligned for it to do so. Only by actively seeking out and taking opportunities can we see our position more entrenched and our moat more resilient. I hope we never lose sight of the bigger picture.

Citations

Singapore’s Stock Market at ‘rock bottom’

Singapore battles to revive struggling stock market

SGX has struggled to find a strong niche

Singapore’s Stock Exchange is aiming to improve its position…

Singapore bonds a low risk diversifier amid uncertainty

Larry Fink’s 2024 Annual Chairman’s Letter to Investors

What has led to Japan’s Comeback

Britain fast-tracks biggest companies listings shake-up in …

Next UK govt needs to divert pension assets, create London’s…

How Japan’s Stock Market reform inspires Asia

Lee Kuan Yew School of Public Policy

Robson Lee: Weak valuations and Liquidity in SGX drive further listings out of Singapore

Singapore gets lion’s share of SEA private equity amid regional decline: Bain Report

Which is the largest stock market in Southeast Asia?

SGX Securities launches world’s first ETF tracking Asia Pacific’s financial sector

Leave a comment