As one can probably tell by now, I’ve been rather annoyed by constant market mispricings of rate cut expectations and retail getting ahead of themselves trying to get the money printer going “brrr” as fast as possible. Is it just me, or do those with no stake in the markets, i.e. the non-traders, the ones that always have the best insights? Seems like when you yourself don’t have a vested interest in short term swings and fluctuations, you are able to best position and analyse fundamentals from a macro view. But anyways, it also seems like global markets and narratives are more so driven by expectations of geopolitical tensions and multipolarity conflicts, presenting a much tougher regime for investors to navigate. Granularity is likely rewarded.

Looking forward, I believe that through all the turbulance there are some fundamentals that remained unchanged. I would love to revisit some of these years down the road just for some laughs and giggles.

Global R* is structurally higher than before, and will stay that way into the next decade

This is something that we’ve talked about before here, and something that we will strongly believe in. I see the Fed’s recent decision to make a shocking 50bps cut in policy rate reflective of the acceptance of a higher neutral rate. Considering the huge economist consensus of a September 25bps cut, I believe the Fed went with the market estimates potentially due to:

- Fiscal Dominance concerns, especially as a wave of sovereign debt is set to mature in the near future

- Fed has lost its independence, and this was a political move (less likely)

- The economy is not as healthy as it seems (possibly, but also less likely because the consumer, corporate earnings and labour markets are robust. October NFP data surprised on the upside as well)

The first of which would indicate that the Fed is likely to accept a higher-for-longer inflation regime in trade-offs with Treasury concerns. No matter the case, structural macro drivers of inflation persist, and will keep costs elevated. We see longer term inflation settling around a 2-2.5% range, barring exogenous shocks and escalation of geopolitical tensions.

Demographics

There’s no turning back the baby shortages — the real question is going to be if AI can yield the much-needed productivity gains such that inflationary demographic spending is accounted for? As Developed Markets (DMs) around the world age and Emerging Markets (EMs) host favourable demographic trends, we see healthcare spending across the board rising in response to increased need for outpatient services, preventive care and palliative care. Even today post Covid, we see healthcare infrastructures as inadequate to respond to the next wave of threats to public health. Nurses are overworked, hospitals are inadequately staffed and climate change plays a conducive role in creating the conditions for new pathogens to send the world into another shock. Even barring the emergence of new pandemics, we believe opportunities lie in drug distributors, who are less constrained by funding and clinical trial risks and yet still stand to gain from increased demand for healthcare. We will keep a close lookout for regulatory developments, especially if Democrats gain control of government levers.

Artificial Intelligence (AI)

This is the big question of the decade and rightfully so. AI winners have been rewarded quickly and huge. Most investors today were old enough to live through the 90s (Japan, Southeast Asia) , 2000-2008 (US) and 2022 (China) to understand how painful asset bubbles can be for the global economy and capital markets, and are desparate to ensure that they do not fall prey to the same frothy valuations once again. Yet forward AI valuations remain modest and earnings remain supported. Fundamentally, AI is an industrial revolution taking place in front of our eyes and huge investments in productive means is always largely beneficial amidst a decline in birth rates and working age populations.

AI itself is likely not as inflationary as we might expect. AI today is a huge water consumer, but in terms of costs and energy, AI itself is getting more efficient and more productive (GPT 4 in 2023 cost $36 per 1 million tokens to run; today GPT 4o costs only $4 per million and its 4o-mini counterpart costs only $0.25). That said, we expect stronger inflationary pressures from increased data center usage as corporations and sovereign nations start to look at the proliferation and utilisation of large data models to increase productivity. The result should be higher inflation from energy demand.

Low-Carbon Transition

This is something we hope to see happen ASAP, and the Russo-Ukraine conflict has been a great push to get most countries onboard. Today renewables are cheap yet electrifying grids and developing electricity capabilities are not. Countries around the world lack adequate infrastructure investments in grid networks and storing capabilities. While we don’t see a phasing out of traditional fuels as possible (and they are also integral to the low-cost carbon transition) due to high dependency on jet fuel and other fuel components, we look towards energy infrastructure opportunities, believing attractiveness in such service providers to be reflected in years to come.

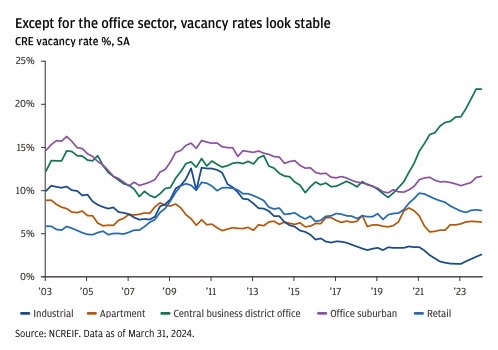

The Dilemmas of Real Estate Exposures

Real Estate is something we are extremely conflicted about (we wouldn’t call ourselves experts on the asset class). In our view:

- Real Estate valuations seem to be bottoming, which might provide a strong overweight case in the tactical horizon

- And opportunities are attractive; we view the Chinese real estate woes to have exaggerated investors fears regarding the cumulative sectoral health, and vastly dampened valuations. There hence is opportunities to capture mispricings

Yet we are deeply concerned about the future of Monetary policy particularly in the US, and how the housing market in particular will be affected by it. We saw how the Residential Real Estate crash in China gave the whole sector a bad rep and thus weigh the structural risks that exposures might bring. In particular, we are worried about fiscal dominance characteristics in the US and how it would affect Central Bank Operations with respect to Mortgage-Backed Securities (MBS) and Credit Levers, in particular through Quantitative Easing (QE) and other Open Market Operations (OMOs).

Into Fiscal Dominance (short)

Fiscal Dominance: A situation when the fiscal authority such as the Treasury faces large current account deficits and debt burdens that leave little room for additional borrowing.

We see fiscal dominance, if it plays out, to be the scenario where the Treasury/Yellen takes precedence in Central Bank decisions. In order to maintain debt sustainability and keep GDP growth strong (for tax receipts), we believe the US will begin to accept elevated inflation with lower policy rates. As a key factor in Fed activity, MBS yields will be impacted.

Some context: the housing market is a key pillar of most economies (hence Fed broadened OMOs to include MBS in 2008). Considering financial institutions (FIs) hold the most MBS exposures, fluctuations in MBS valuations can lead to inflated balance sheet losses and stress on the financial system. As compared to if the Fed were to purchase corporate debt to stabilise companies, the housing market also directly affects consumer wealth, banks and overall economic confidence. Stabilising the housing market through MBS and OMOs has a more direct, widespread and immediate impact on the financial system. This is why alongside US Treasuries (USTs), MBS are the choice security for Fed activity.

We view hastiness in easing with a 50bps cut as a possibility of a need to position before a wave of sovereign debt maturity in the US, rather than getting ahead of the curve amidst strong consumer data, spending and corporate earnings. A strong cut in October would further entrench our market view of a fiscal dominance scenario.

Hypothetical Fiscal Dominance Playing Out (Bear Case)

- The Fed no longer operates solely on their dual mandate, and operates in consideration of the Treasury’s priority for fiscal sustainability. Inflation will be allowed to band higher than current target levels

- Policy rate to be fixed lower

- Through the Signalling effect and increased institutional concern over fiscal health, we see another downgrade to UST credit ratings or investors look for alternative investments. Subsequent bond purchases would involve stakeholders that demand higher yield premiums in excess of auction yields, and rates in secondary markets rise

- To ensure that primary auctions do not fail when expected rate > Treasury target rate, the Fed conducts large scale OMOs to replace sovereign/institutional/retail debt purchases. Lower sovereign purchases of US debt is already taking place

- OMOs and UST purchases are funded through money creation, and US M2 expands meaningfully. This drives inflation higher and further entrenches a rise in price levels

- The Fed is forced to persistently conduct Yield Curve Control (YCC), leading to heavy distortions in the sovereign debt market and reducing market participants

There are some considerations before we all head for the bunkers and go risk-off US debt exposures, which further add to our conflicting thoughts.

- At what stage do investors deem fiscal health of the US to be unbearable, eroding their safe haven status?

- Allowing fiscal dominance to occur is likely politically unfeasable, especially when politicians prioritise electoral outcomes over long term health of the country

- We talk about structurally higher inflation — how possible is YCC even during inflationary environments?

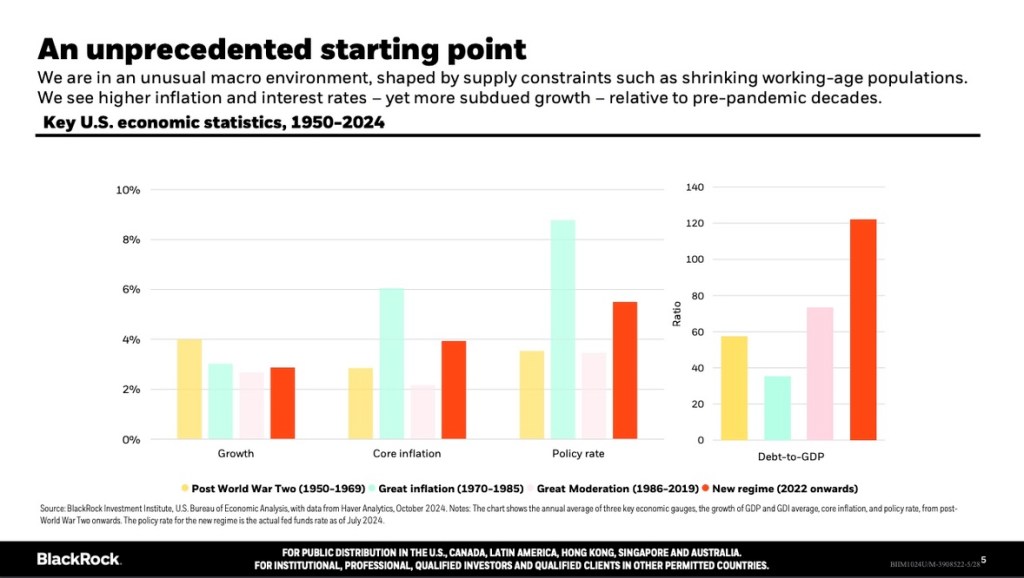

Yet we also see institutional concern regarding fiscal sustainability and inflationary pressures being more pronounced — slowly yet surely. Take a look at this Blackrock brief done recently to investors:

We all agree that the US will never allow debt defaults, which would severely undermine Basel III assumptions and change global perceptions of what constitutes High Quality Liquid Assets (HQLAs), leading to unprecedented stress in the global sovereign debt market. As such, we believe a hybrid fiscal/monetary dominance situation. How this likely plays out is that the Fed still deviates from independence and acts with Treasury considerations.

A lack of bipartisanship and political fragmentation makes resolving fiscal deficit issues even harder (we are already enduring the highest fiscal deficits in peacetime today!) especially with large sums of government spending in nondiscretionary areas. A reduction in spending in key welfare programmes is likely impossible due to political unpopularity. On the other hand, the US has also an amazing case study in its closest region and knows the dangers of taking on austerity measures and stifling investment.

In summary, a combination of entrenched inflationary pressures, subdued growth with a retreat in trade liberalisation globally does not prove to be a favourable outlook for bond holders.

The Hybrid Model

This is our most probable case regarding longer term Monetary Policy:

- The US continues to raise the debt ceiling indefinitely

- A hybrid model for fiscal/monetary dominance becomes the mainstay. Policy rates are kept lower than r* through OMOs. Sovereign debt and MBS yields are distorted and do not reflect true market pricings, as the Fed is forced to intervene protractedly in the debt markets

- The Fed will be more accepting of elevated but controlled inflation. Policy rates are unlikely to hit past highs, while there is no restrictions on ultra-accomodative monetary policy during downturns. Longer term rates band lower than historical averages. This represents a deviation from Central Bank independence

- US M2 still increases as the Fed continues to conduct OMOs, but stops short at outright YCC

Long or Not?

The confluence of factors above drive a preference for agency MBS. We deliberate leaning into residential real estate exposures.

We see tailwinds for homeowners especially with the proliferation of advisory services, expecting the housing market to stay competitive. Firms such as RealPage coordinate with landlords in cities across the US to prioritise higher rents and accept lower occupancy rates. The result has been an increase in profitability in home ownership as a commodity and we believe this translates in the valuations.

Relatively lower MBS rates and hence mortgage rates potentially drive interest in homeownership. As immigration numbers keep housing and rental markets tight, we expect housing valuations to be propped as well as investors are incentivised to borrow. This effect might be more pronounced in EMs with higher population growth.

We expect construction costs to rise, providing further tailwinds for home prices and headwinds for mortgage deals. Ongoing challenges in housing supply due to elevated material costs and labour shortages are exacerbating price increases and pricing out market participants.

Yet elevated inflation could erode real incomes over time, resulting in a higher savings rate and reluctance to take on new debt or make spending due to the wealth effect. A reduction in longer term purchasing power hinders our valuation growth. Rising home values may also lead to elevated property taxes, affecting homeowners’ expenses.

Higher costs associated with factor inputs are also expected to drive up upfront costs and impacting project profitability. Even as strong demand and favourable conditions incentivise the provision of supply of houses, supply chain constraints could pose challenges.

Overall, we expect housing valuations to rise meaningfully, fueled by inflationary pressures and ease of credit.

Risks

Yet we see potential systemic risks growing in the housing market on a strategic horizon. These are driven by:

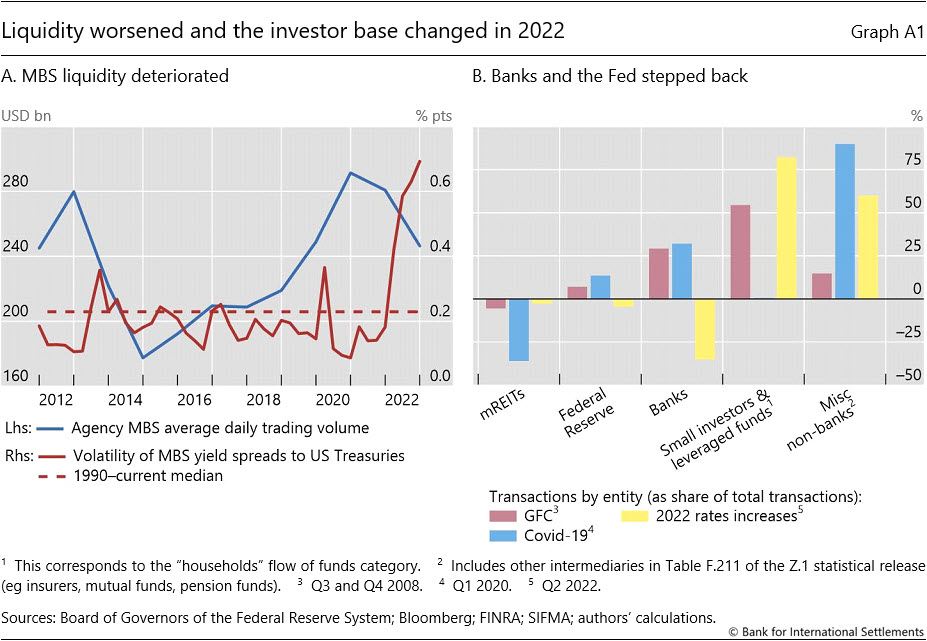

Distorted Risk Premiums as MBS rates stay lower than true market pricing and underlying credit risks are masked. The present Japanese Government Bond (JGB) market is a prime example of market distortion due to Central Bank activities and extensive ownership of existing supply.

Potential Moral Hazard with speculators expecting the Fed to persistently intervene in the housing market. We have learnt enough from the Japan of the 80s, Asia of the 90s, the US and China to know that eased credit conditions and higher monetary supply with potentially higher collateral multipliers can lead to painful asset bubble bursts. The Fed must ensure it does not become a “dealer of last resort”. The risk on moral hazards is huge — during times of heavy Fed intervention such as the Covid-19 crisis, Fed activities aimed at suppressing yields heavily incentivised borrowers to take on excessive debt by offering attractive, low-cost financing through MBS which boosted housing demand artificially even as prices rose due to inflationary pressures. Divergences in forward-cash basis (price difference between to-be-announced contracts and specified pool contracts) also widened significantly in March 2020 due to MBS market liquidity constraints. Such risk mispricings could lead to overextension of borrowers who are enticed by low rates, but during normalisations, defaults can surge as not many are able to service their debt. Balance sheet constraints as a result of moral hazard due to regulations such as the Supplemental Leverage Ratio (SLR) also limits dealers’ abilities to absorb MBS. If borrowers were to default en masse, their balance sheets could be overwhelmed, forcing a further sell-off and downward pressure on MBS prices, exacerbating a liquidity crisis.

Elevated Refinancing Risks. In our hybrid fiscal/monetary scenario we observe limited upside to rates during inflationary pressures and stronger downside during recessionary pressures as the Fed is less constrained by how low policy rates can be, as long as they remain positive. If financial institutions were to take on higher MBS exposures and investors engaged in speculative and transactional purchases of residential real estate, we see a 90s Japan scenario likely to happen during downturns, where credit lending dried as banks faced larger losses and held back lending even for productive means even as yields became lower. Economists were left baffled at the extent of the recession in Japan, considering how dominant the Japanese economic model was years prior.

Excessive Hidden Leverage in the shadow banking system. Entities such as mortgage real estate investment trusts (mREITs) and hedge funds are less regulated than traditional banks and operate with significant leverage. They often finance long-term MBS holdings with short term repo transactions, creating systemic risks especially during times of crisis where liquidity in the MBS market dries up as these entities are forced to fire-sell their positions to meet short-term funding obligations. The Fed is subsequently forced into becoming a permanent “dealer of last resort” to prevent a collapse in the MBS market and stabilising valuations.

Looking Outwards

As we’ve always said, we are now living in a world of unprecedented uncertainty and a rejection of prior trade liberalist principles (interestingly, it seems that China is now the one preaching open borders and engaging the world?). The resultant lack of clarity in global policies influences our preference for robust structural macro drivers such as Demographics and the Low-Carbon transition. Like mentioned, we see opportunities in the drug distribution sector as well as in energy infrastructure projects.

We are at an impasse on the real estate sector, noting the mispricing opportunities bearish investor sentiment brought. We note the potential for meaningful capital appreciation on a longer term horizon as our forecasted hybrid model comes into play as we end the decade, whilst ensuring we stay updated with the as stated above risks.

Leave a comment