The world today is one marked by profound transformative developments as the global landscape continues to evolve at a blistering pace. As a global long term investor, we must contextualise the structural undercurrents and navigate the changing tides amidst the global landscape and geopolitical recession we find ourselves in. Each of these structural changes carries significant implications for investors and global communities, and we often forget the best means to secure long term, meaningful risk-adjusted returns is to leave the world a better place for the future today. This means taking an active Apollonian involvement in things that seem out of our purview — the political process, the tolerance of diverse viewpoints and encouraging genuine dialogues.

3 months into the new Administration in the US, I thought it apt to deliberate some of the biggest Gray Rhinos of today, which represent clear risks to the global landscape we have come to love but are grossly underrepresented in discourse. Resolving and tackling each of these also represent cutting the Gordian knot, due to increasing complexities towards bipartisanship and coherence.

Table of Contents

- The Growth of Private Market Opportunities

- The Technological Ascent of China and its Autarky

- America First Alone

- The Enactment of Barriers

- Myths and Realities of US Exceptionalism

- The Hegemonic Stability Theory

- The Erosion of Democratic Norms

- The Great Wealth Transfer

- Navigating the Decade Ahead

The Growth of Private Market Opportunities

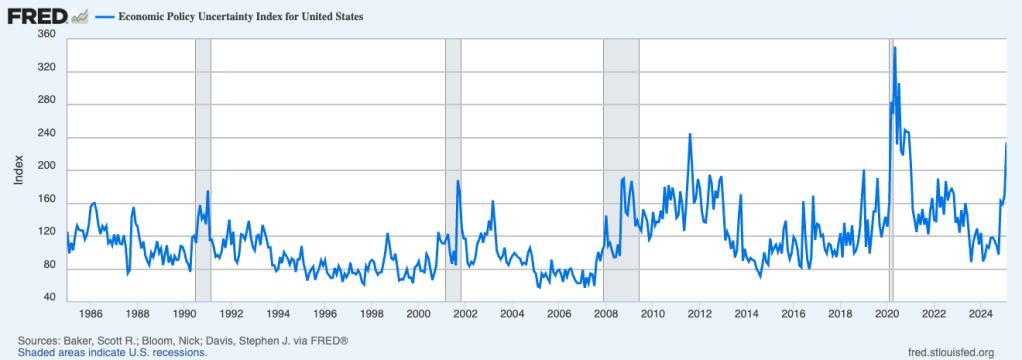

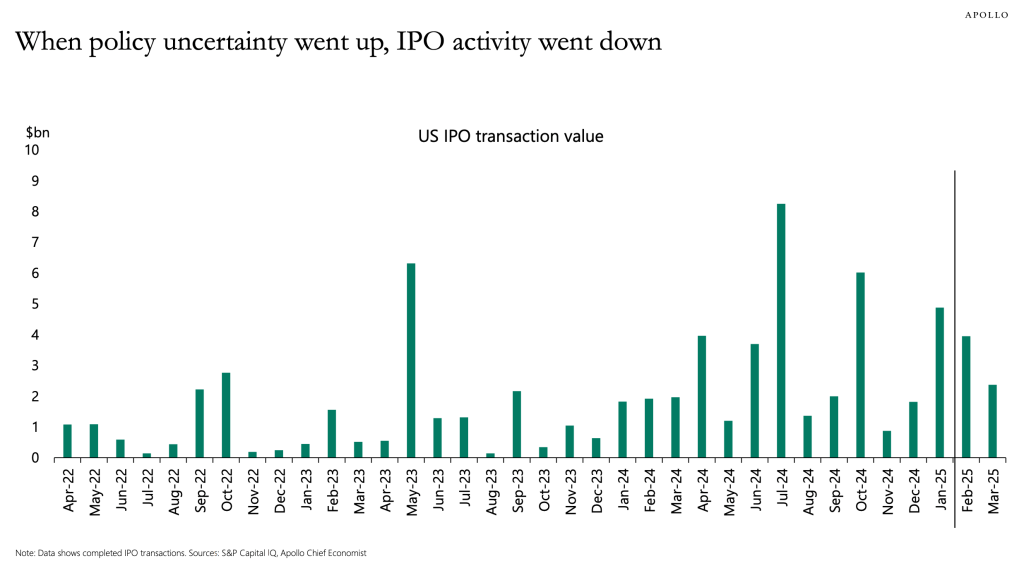

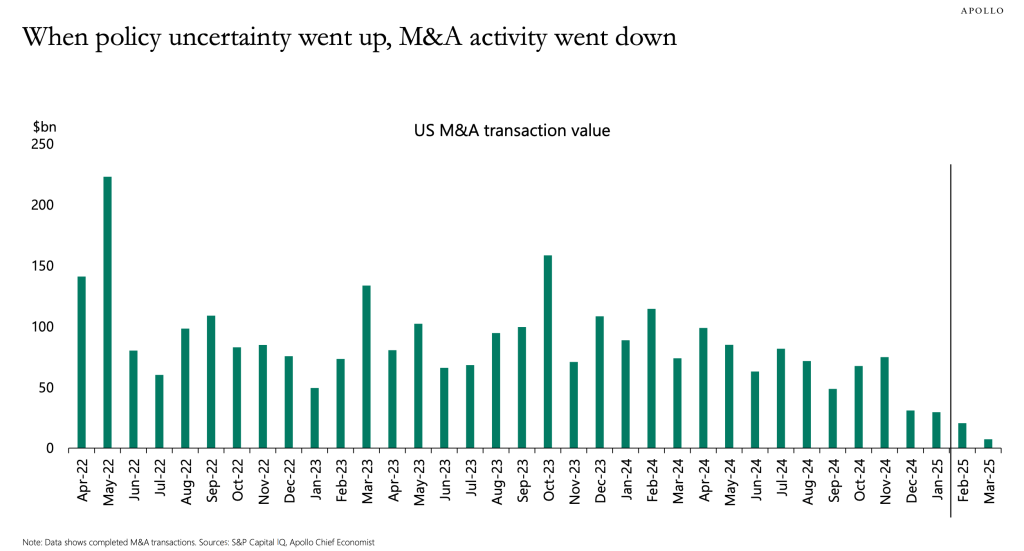

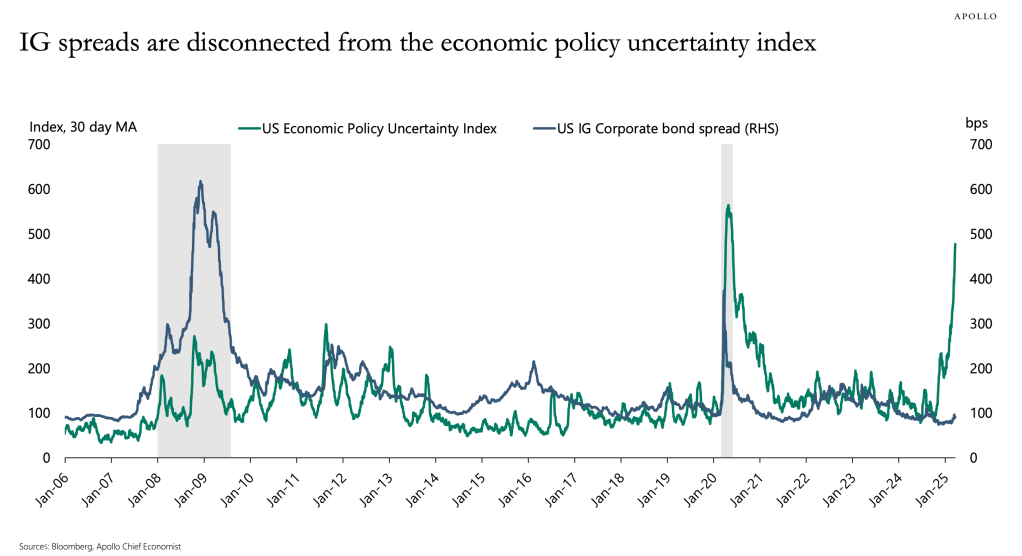

The ambivalence surrounding the higher-for-longer rates environment, elevated uncertainty (at levels only observed during the Great Financial Crisis and the Covid-19 Pandemic), with yet a continuation of the historic spread compressions has been off-putting for investors particularly in the private markets, particularly those who have been looking for attractive exit opportunities presumed to arrive in the Trump Administration. Exit multiples continue to stay in line with decades trends, we see a contraction in the PMI and Consumer Confidence, and a wait-and-see attitude that is damaging the performance of GPs.

How have GPs continued to ensure adequate distributions to their LPs? During the lull of the rates environment, a re-emergence of dividend recapitalisation in private equity has seen to a 71% increase in such transactions in 2023 on the year, with the frequency of such deals also continuing to grow.

A trendline of building up balance sheets during a period of elevated financing costs to mitigate an unattractive exit environment to urgently return capital to LPs is itself significant. There is a way to look at it — GPs are perhaps confident in the macro outlook and betting on dealmaking to benefit from the arrival of near term tailwinds hence a willingness to raise leverage and heighten their portfolio credit risk. This is essentially a bet on the strength of future cash flows against the discount, and professionals must balance the short-term appeal and demands of providing immediate cash distributions against the long term health and sustainability of the sector and businesses they own.

Moreover, it is neither comforting to note that Moody’s conventionally downgrades companies after debt-funded dividends are paid, recognising the negative impact on companies’ financial profile. The near term economic outlook is neither one of rosiness and clarity — the EV/EBITDA ratios remain largely in line with historic trends whilst the Fed Funds Rates remains sticky; consumer sentiment dips and IPO frequency fails to buoy. Continued jingoism by the United States towards its allies, threats and trade tensions create greater headwinds towards generating attractive macro conditions in the near term, and Trump has also acknowledged there would be harsher conditions for the time being.

The resurgence of debt-fueled distributions warrants a closer look at the underlying strength of the economic conditions, covenant protections and debt cushions in leveraged loans and high-yield bonds as we monitor the sustainability of debt loads in a world I’ve continually argued to be one of structurally higher costs of credit. Ultimately, I do not believe the rosy financial outlook justifies the added-on risk behind debt-financed distributions, and risks sandwiching GPs between obligations to clients and lenders.

But just as important as the understanding of debt obligations and capital structures is the cultivation of a global, interdisciplinary worldview — all the more pertinent in private markets. We are exiting a world of secular stagnation and extremely accommodative capital costs meant to assist businesses and firms rebuild their balance sheets post-GFC, which also means exiting the comfortable conditions of one tide lifting all boats. Granularity and activeness towards allocations are going to be more critical, and firms can no longer expect beta to drive significant returns.

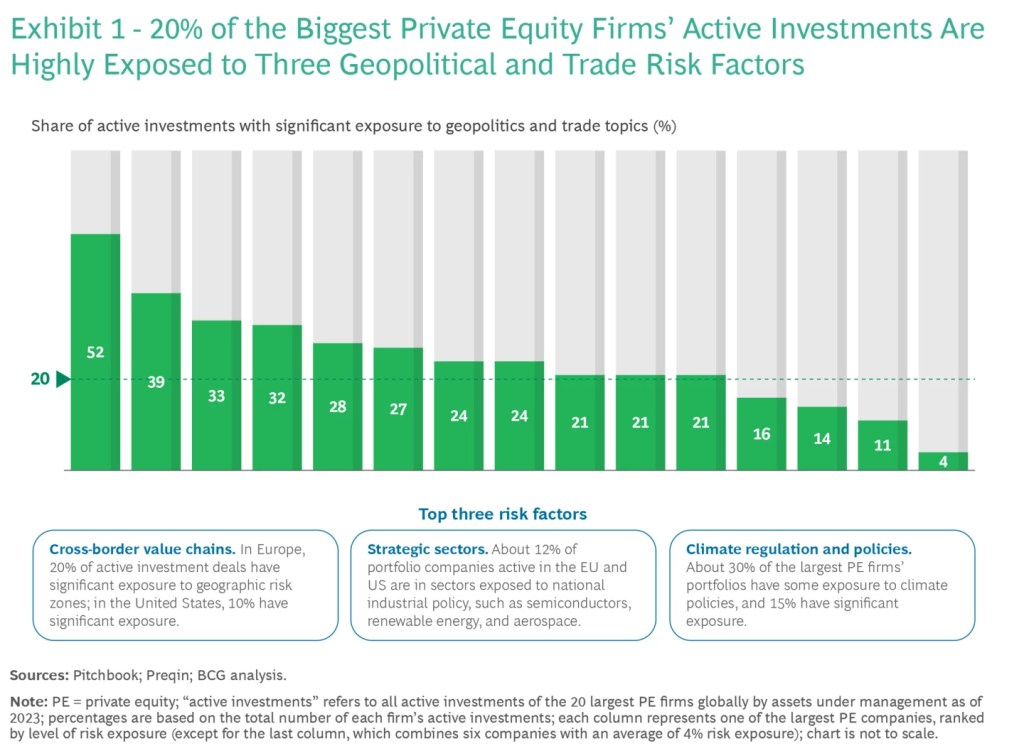

Private markets inherently subject GPs to greater discipline and risk management than the public markets where investors can cut losses and move in and out of positions intraday, within weeks or months; whilst Private market opportunities are illiquid and held up for longer. What this means is that fundamental forces, such as rate cycles, geopolitical and regulatory divergences, supply chain dynamics and political developments shape the landscape that leveraged investors are looking to exit in ten years down the road. A recent analysis by BCG found that 20% of the largest PE funds are exposed to significant geopolitical and trade risks, yet most have not invested as significantly in “geopolitical muscle” nearly as much as the animal spirits drove them to rapidly expand business function. As much as technicals, financial understandings are critical within the investment landscape, it is naive to believe that a manager who lacks active involvement and understanding of the multidisciplinary world will be able to adequately understand the climate he tries to exit in, a decade later.

As a long term thematic investor, we are constantly looking to hone our grounding in how global systems interact. This means implementing a conscientious blending of our financial and granular acumen with the knowledge of political developments, history, scientific breakthroughs and cultures. I believe that only with understanding communities and the human spirit can we continually filter impractical traps from attractive opportunities. Take for example, telehealth solution providers in India who saw a huge market and a strong need for equitable and permissable health interventions for families. An investor who has not bothered to understand the cultural and social nuances of India would have opined that the telehealth services offer a once-in-a-lifetime panacea and lucrative investment opportunity that is too good to be true — and it is. India, although hugely cultural diverse and home to a broad set of very different norms between states, operates largely on trust. Visiting a doctor in India is done as a family, and the people there value the human touch and trust provided by certified health specialists, which telehealth cannot adequately provide.

In short, the resurgence of dividend recap practices is merely a microcosm of the larger theme that has to surround private markets moving forward: short terminism must be weighted against long term systemic understanding. To drive long term sustainable returns is to break out of silos, invest in our global understanding and being present. This remains especially pertinent in areas such as Europe where private investment is likely to drive 80% of financing needed; anything less than a robust risk framework and code of ethics means significant implications on the real economy, businesses and way of living.

The Technological Ascent of China and its Autarky

The one who establishes dominance during periods of great technological change, writes the new global order

The decisive decade of competition between the increasingly-alone US and China plays out across several vectors, including soft power, militaristic influence, domestic currency proliferation, and more. None are as intense as the arms race in advanced technologies.

The revelation and coining of the “DeepSeek moment” earlier this year draws personal ire, particularly when hearing sentiments regarding how China was able to innovate in this way, or propose with certainty but no backing there must have been fraud involved. The ability itself to be stunned that such innovation arose from China happens to also be incredibly Eurocentric and reflects the excessive hubris and epistemological bias that has revolved arond the general public in the past decade.

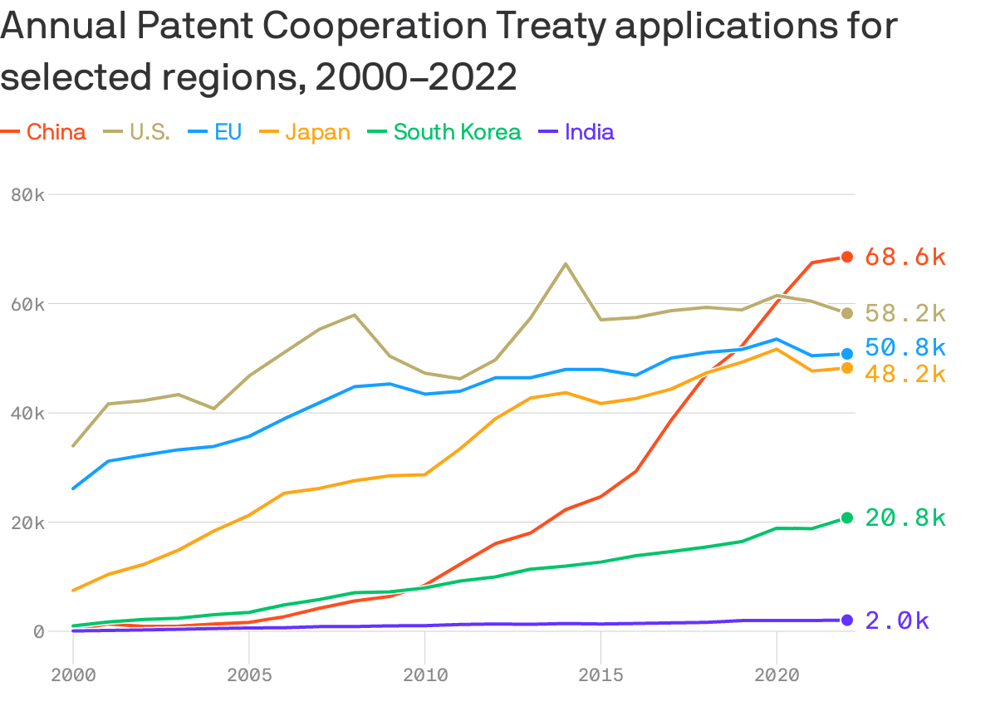

Why is such innovation not shocking? Within the past decade, China has overtaken the US in international patent fillings and seen its AI-related patents balloon from 650 in 2012 to over 40,000 by 2022 — approximately four times that of the US. China today leads the world in AI patent output, especially in areas including machine learning and computer vision.

Chinese innovation is not limited to AI either; China today boasts the world’s largest quantum communications network and publishes more quantum research than any other nation since 2022 including the US and leads in practical quantum communications and sensing applications, with over $15 billion in public quantum funding (far outpacing the US).

What does this mean? Firstly, it is that underestimating China sets any investor (or other member of the global community) decades back in understanding. Secondly, innovation is no longer synonymous only with Western economies — China’s meteoric rise in cutting-edge frontiers such as AI, quantum, biotechnologies, advanced materials means that the next decade’s disruptive companies will continue, if not more often than not, from Shanghai or Shenzhen as Silicon Valley. The investment implication is important and forces us to broaden out our alpha opportunity set; this could mean increasing exposures to leading innovators and creative solution providers in different parts of the world, while also staying abreast of development trends especially in China, where creativity and change quickly influence global value chains.

This is not to say the driving tenets of US exceptionalism and strength have faded. The US still retains the deepest, most liquid capital markets with robust regulatory frameworks that maintain it the most attractive place to scale an enterprise; the US still is home to world class universities, a strong entrepreneurial scene and the most lavish venture capital markets with strong animal spirits. But the US will see itself running into an unsurmountable Chinese ecosystem in the very near future if its government decides that belt tightening in research and university grants is the anecdote to Chinese state-backed, mission-oriented innovation and credit allocation. It will continue to struggle and lose share in the patents and research landscape if it continues to educate foreign researchers in its universities, but makes obtaining work visas for these talents almost impossible, sending them back to another country to push their scientific boundaries there.

Today, China is pushing forward in a great many areas with the goal of technological self-sustenance in advanced technologies, especially in areas where the US-led Pax Americana has defaulted to coercion and export controls to stymie Chinese growth. We see this in the US CHIPS Act, Europe’s digital sovereignty initiatives as export controls, sanctions and investment restrictions begin to shape and fragment the scientific and discovery landscape we live in. Decades ago, the porous nature of scientific discoveries was immutable and the world benefitted greatly from continued global engagement and cooperation. Great power rivalries today threaten to ossifiy a state of bifurcated markets and developmental pathways, which itself hosts an outcome no one can predict (separate technological standards, types of developments or ecosystems).

At the same time, patent figures do not translate to a definite technological and industrial edge, especially with China’s patent strategy focusing on quantity and emphasis on number of applications. And whilst we must absolutely not demean the tremendous strides China has taken within recent years, we look to the play-out of the Industrial Revolution and understand it is not just who develops the best and fastest, but who leverages and utilises it the best and fastest (Britain sparked the Industrial Revolution, but the US adopted the innovations to the mainstream fastest). We look towards growth regions that provide favourable regulatory environments and societies acceptive towards novel innovations for investable opportunities. Holistically, the Chinese innovation and patent strategy, coupled with their open-sourced proliferation resemble their approach towarads the internationalisation of the Renminbi through mutually beneficial financing via the One Belt, One Road initiative. That’s how we believe internationalisation and adoption occurs; through beneficial transactions, not unilateral decisions.

Moving forward, our portfolio strategies will reflect the reality of a multipolar and innovative world. We aim to capture upside from innovation wherever it occurs and remain open and informed on global opportunities in an unbiased manner.

America First Alone

The US has always acted on its interests, and conflicts and disagreements with allies is not a recent phenomenon. Yet, recent phenomenon which include continuous and escalating threats to Canadian and Greenland’s sovereignty, persistent disrespect towards allied leaders and an outright support for opposition parties in Europe has deviated from what should be acceptable by the leader of the free world.

Trust itself is fundamental to a rules-based world order and is not easily re-established once broken. Already, allies and NATO countries are claiming the relationships they have had with the US “over”, are pulling out of previous arrangements, or are actively looking towards alternative arrangements. Make no mistake, the appetite for global integration and cooperation stays strong — the EU continues to look towards regional partnerships and FTAs with blocs including Mercosur; Singapore just signed the first Comprehensive Strategic Partnership with a Southeast Asian nation. The only difference is today, alliances and commitments with the US are considered not just strategic benefits, but also points of vulnerabilities. There will be no easy unwinding to the damage the current administration is doing to the US soft power, just as much potential allies will be unsure if maximalist jingoism will not return to the Office of the President.

The cumulative result will be a fragmented world where geopolitical considerations and risk become the fundamental and primary driver of investment risk. Going back to the earlier point made on private markets, I would like to expand this to a universality here. There should be no enterprise or institution serving global clients that is not investing heavily in its global touch — this means building on its geopolitical muscle and brains that follow developments closely.

History shows that the interregnums of Great Power transitions last decades or even centuries. Within our lifetimes, the consequence of the American violent pullback will not happen at a tectonic scale. Yet this doesn’t mean that we blindly believe the US markets will continue to be the primary source of returns for the next decades and risk obfuscating the thematic and long term lens needed to drive outsized returns.

Amidst these bouts of heightened uncertainty and tensions, some of what the US is pursuing can be viewed as legitimate issues of concern, not limited to the contested hollowing out of the American industrial base and stripping the US bare to just a financial centre. I advise giving this Twitter thread a read:

The Enactment of Barriers

Globalisation as we knew and enjoyed is evolving. Over the last decade, trade barriers and protectionist policies favouring regionalisation and domestic supply chains dominated headlines, whilst capital barriers received less of the limelight. Today, we are seeing a marked increase in regional regulatory divergences and capital controls, indicating that the friction in cross-border capital movement is rising. Trade openness has plateaued since the Global Financial Crisis, while cross-border assets have trended downwards or sideways since the Covid-19 pandemic and the Russo-Ukrainian conflict.

A stark manifestation of this phenomena is the return of capital flow management measures in various forms. A decade ago, many countries hedged against external shocks and Dollar tightening by accumulating foreign exchange reserves and imposing capital controls; fast forward a decade later policymakers are increasingly leveraging the use of tools of economic statecraft ostensibly to protect national interests, fragmenting the free flow of capital in the process.

At the same time, regulatory divergences inter and intra-region is growing. We see this in divergent approaches to financial regulation (i.e. the uneven implementation of Basel 3 banking rules, the proposed EMIR 3.0) and in market access rules. Nearer to home, multinational companies and investors face a patchwork of rules, necessitating higher compliance costs, uncertainties and aversion to the interoperability of capital internationally.

There are several concrete observations to note here:

- The World Economic Forum notes rising geopolitical tensions and fragmentation could cost as much as 5% of global GDP in lost economic output.

- Increased fickleness in cross-border portfolio flows, especially in geopolitically sensitive regions.

- The codification of preferential blocs due to the declining meaning of Permanent Normal Trade Relations and the WTO.

The implications for investors are multifaceted and complicated. These factors could mean lower trend growth and suppressed returns at the benchmark level, greater geopolitical risk and regulatory uncertainty that hamper investment decisions and risk setting the world on a path of compressed risk taking activities. Moreover, the emergence of preferential blocs with potentially separate payment systems, invoiced currencies and trade networks pose headwinds to strategically non-aligned countries that are omitted from favourable treatments, potentially pushing these countries to take sides in the power rivalry.

Such changes while monumental in nature, also provide investors with plenty of opportunities to deploy capital with local expertise and get rewarded. Certain countries that implement such barriers to capital movement often develop their domestic capital markets more vigourously to reduce dependence on foreign inflows, such as through the encouragement of domestic institutitonal investors in local bond markets. We will continue to closely monitor developments in markets like India, where huge consumer bases, strong retail investor participation and favourable youth demographics coupled with reforms creates opportunities; or the Gulf countries, who are attracting sizeable financial inflows as they aim to become a financial powerhouse.

As an Asset Manager that deploys in the strategic horizon, these trends reinforce our belief for the need for geographic diversification and active portfolios. We can no longer assume frictionless and permissive market structures and fund environments across regions, and must continue to leverage local expertise to bridge the knowledge gap especially in emerging markets where opportunities are plenty. The emergence of bloc-alignment also means currency strategies must evolve to constantly evaluate the costs of jurisdictional risk.

Holistically, the enactment of barriers and frictioned trade means a tougher returns environment for fund managers to create returns because of a compression of higher downside and stunted upside risk. This necessitates a premium allocated towards policy analysis as part of investment research, including how the direction of regulations impacts exposures in different environments. Whilst regionalisation becomes a key theme of the 21st century, our job as proactive and engaged global investors stays the same. We will continue to stay diversified across themes and geographies, and navigate the vertiginous tides through avoiding taking all-or-nothing bets on the future.

Lastly, we should reconsider the roles of Bretton-Woods institutions in this changing landscape. The IMF’s role as a global financial stabiliser is being tested as countries look towards bilateral swaps and regional financing arrangements. As such movements are made due to weakness in the global coordinated system, we should be expecting future financial crises to be tougher and more entrenched than before, with fewer coordinated bailouts. Whilst the US understood the importance of international solvency and opened significant bilateral swap lines and foreign repo funds, we cannot expect international cooperation or the global lender-of-last resort to work the same again.

Myths and Realities of US Exceptionalism

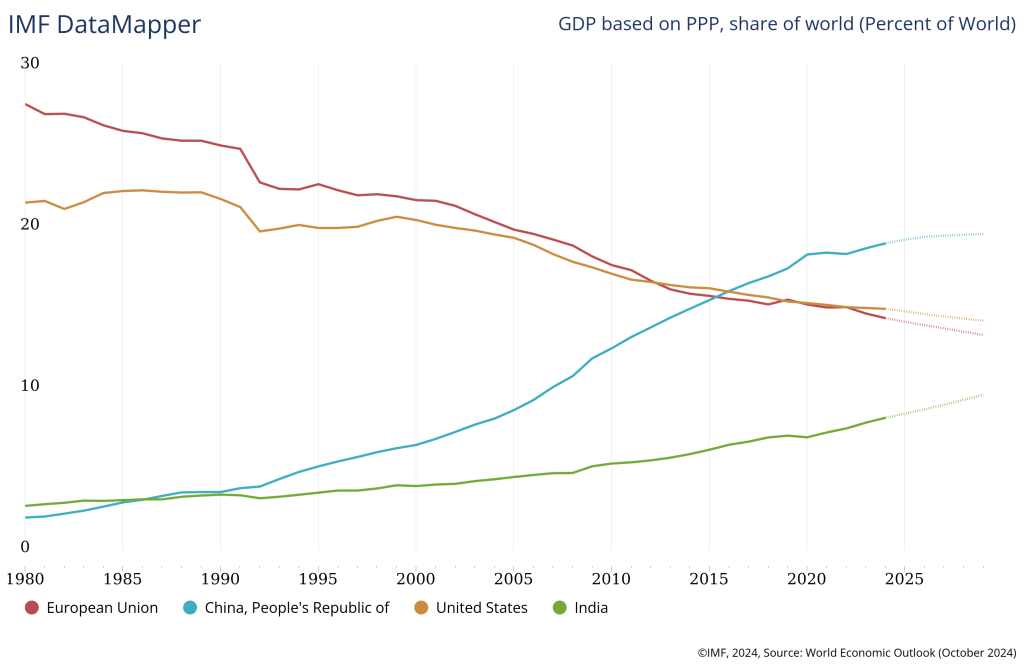

By many quantitative measures, the US’ share of global predominance has declined from the past, with an approximate 16% fall in global share since 1960. This is not indicative of US flatlining growth but strong emerging markets economic growth on the back of the free international trade and liberalisation policies. In technology as discussed earlier, the US can no longer expect unfettered dominance in key areas such as AI patents or quantum research; capital markets remains in the hands of the US’ global lead with around 55% of global equity market capitalisation and status as the reserve currency issuer, but even here we are seeing gradual but seismic shifts to US primacy.

What is often misconstrued around this topic of contention is the notion that fading exceptionalism equates to an immediate irrelevance or inevitable free fall; such a construct neglects enduring pillars of American strength: robust regulatory frameworks, entrepreneurial ecosystem, demographic openness (or attrativeness), a culture of innovation, deep financial markets and a network of alliances still, because the alternative to an American-led global order is one that is much less attractive to most Western nations. While China may surpass the US in global GDP share, the US’ alignment with other economies (EU, Japan, Korea) means it continues to exert strategic influences in different spheres around the world, forming a powerful coalition that still commands much of the global technological prowess and innovation. The resilience and dependence on military alliances means the US will continue to leverage a reach no other country will have. The frameworks for thinking about the US role hence should not be one of a either-or dyad, but about the world moving away from an ephemeral period of solo hegemony post-Cold war towards a multipolarity with near-equals.

In addition, I believe the right way to be looking at the foundational changes of today is through the separation of absolute from relative strength.

What is happening currently is what we would call foundational uncertainty because this uncertainty touches on the very foundation of what we have been standing on and building on for many decades. This would include things like the world order

~ Lim Chow Kiat, CEO, GIC.

In absolute terms, the US will continue to grow its economy, maintain the most conducive environment for corporate and business risk-taking activity and perhaps strengthen its institutions; and in relative terms, the rest of the world catching up, which is not insofar as to the American decline as the rise of the rest (critically, on the waves of American foundations). This convergence is instead a sign of global developmental success; we have seen hundreds of millions lifted from poverty, the creation of new centres of excellence and democratisation of access to institutions and opportunities. Today, Chinese analysts continue to study and respect sources of US power, recognising the different areas where US dominance remains unparalleled.

Historical precedents are also of importance to our contextualisation as global long term investors. The US is not the first global power to face a relative decline, nor is the Dollar the first currency to face its challenges (think the Spanish Silver, Dutch Guilder and the British Pound). These periods show that a nation can remain influential and prosperous even after it is no longer the singularity on the global arena, but only if it adapts its strategy. For the US, adapting likely means doubling down on its strengths, its ideas and continuing to engage the democracies across borders who have their prosperities and defense strongly intertwined with American exceptionalism. It also means investing heavily in its human and productive capital: university grants, upholding of the rule of law, openness and uplifting communities through investing in the environment (renewable energy sources, infrastructure, firm energy grids, and clean water access). I bring this up in an investment thesis because of how the financial economy is deeply shaped by the currents of the real economy.

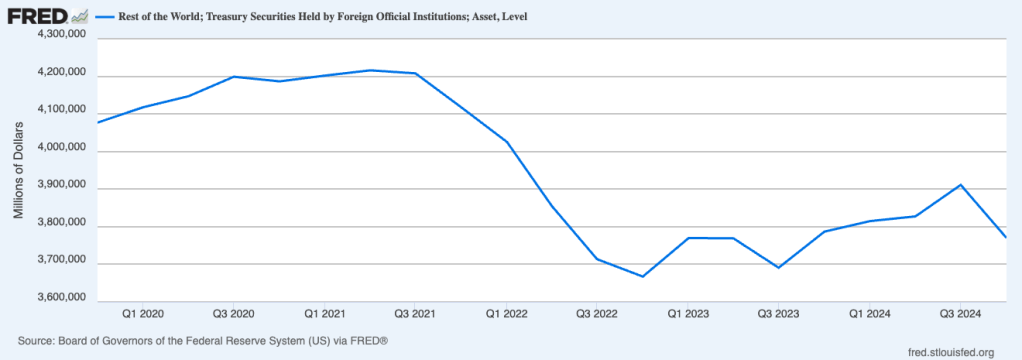

From an investor’s perspective, the fading US exceptionalism has concrete effects on asset allocations positioning as we look well into the future. The post-GFC era was earmarked by US asset outperformance: their equities led international counterparts, the Dollar strengthened and they produced the most trillion-dollar market cap and unicorns in the world. This outperformance was buttressed by ultra-accommodative monetary stance, regional weaknesses (sovereign debt crisis in Europe, regulatory crackdowns in China, etc) which supported the case for higher portfolio US concentration as a source of outsized returns and a safe haven when financial conditions tightened. Some of these, including the era of low-rates and high credit impulse have perhaps unwound, which means we could see more non-US assets in portfolios and become key sources of diversified returns. Just earlier this year, UBS warned that fading US exceptionalism could put over $14 trillion of unhedged assets at risk as global investors look to rebalance their overweights in US equities, and a 5% reduction in foreign holding of US assets would imply a $700 billion in outflows, on the order of two-thirds of the US annual current account deficits. In practical terms, this means the US who grapples with a pullback in marginal price-inelastic foreign Treasury buyers and reduced attractiveness of capital markets, could see downward pressures on their Dollar over time and heightened difficulty in maintaining a balance in their current and financial accounts. The Dollar’s value is of course multi-determined, but I believe the ability to continually finance deficits and uphold trust in the Dollar’s reserve currency status has been largely due to the strength of American corporates and capital markets.

This again segues into the overarching theme that I have been contending upon for much of this article: the need to broaden our opportunity set and earn attractive diversification dividends. Investors today are rightly concerned with the US concentration of their portfolios, but even this counter-cyclical move could be self-reinforcing. This does not mean abandoning the most lucrative markets in the world with public and private companies with tremendous earnings power and margin retainment, but it does mean opportunities in themes across regions, such as demographics in Indonesia and Sub-Sarahan Africa; energy and defense in Europe, and digitalisation in Asia-Pacific justify increasing our international exposures. We also favour emerging market assets especially in countries looking to form stronger regional partnerships, and like what we see in financials as they tend to capture nominal growth better. A multipolar world implies that economic leadership will be shared, hence should our investments.

It is also important to apply the right risk frameworks and stay informed regarding developments within the US. The financial system and Treasuries remain the global anchor, but we keep acutely aware of mounting stresses in the system and the potential for failed bond auctions or political gridlock. Ultimately, the appropriate risk framework avoids two extremes: complacencies over US continued outperformance, and doomism. The reality for the strategic horizon likely involves the US markets remaining a cornerstone of significant investment returns and portfolio allocations but no longer the only pillar. By thinking in systems, of which the US is one part of a larger, diverse global network, we can better anticipate how shocks and black swan events propagate.

The Hegemonic Stability Theory

The hegemonic stabilty theory posits that international systems are most stbale when a hegemon exists, as this hegemon provides leadership and stability through economic and political means.

We have continued to reiterate our belief for the existence of a multipolar world with no clear cut hegemon. In this scenario, several powers including the US, China, the EU, India and other fringe global powers like Japan will each hold significant sway, but none will dominate the global landscape.

The world has entered a period of heightened competition and is marked by techno-nationalistic industrial policies. We anticipate more regional champions to emerge in different fields, such as Indian tech and servies scaling up to rival regional counterparts, or European clean energy. This forms the basis of our preference for themes, across geographies.

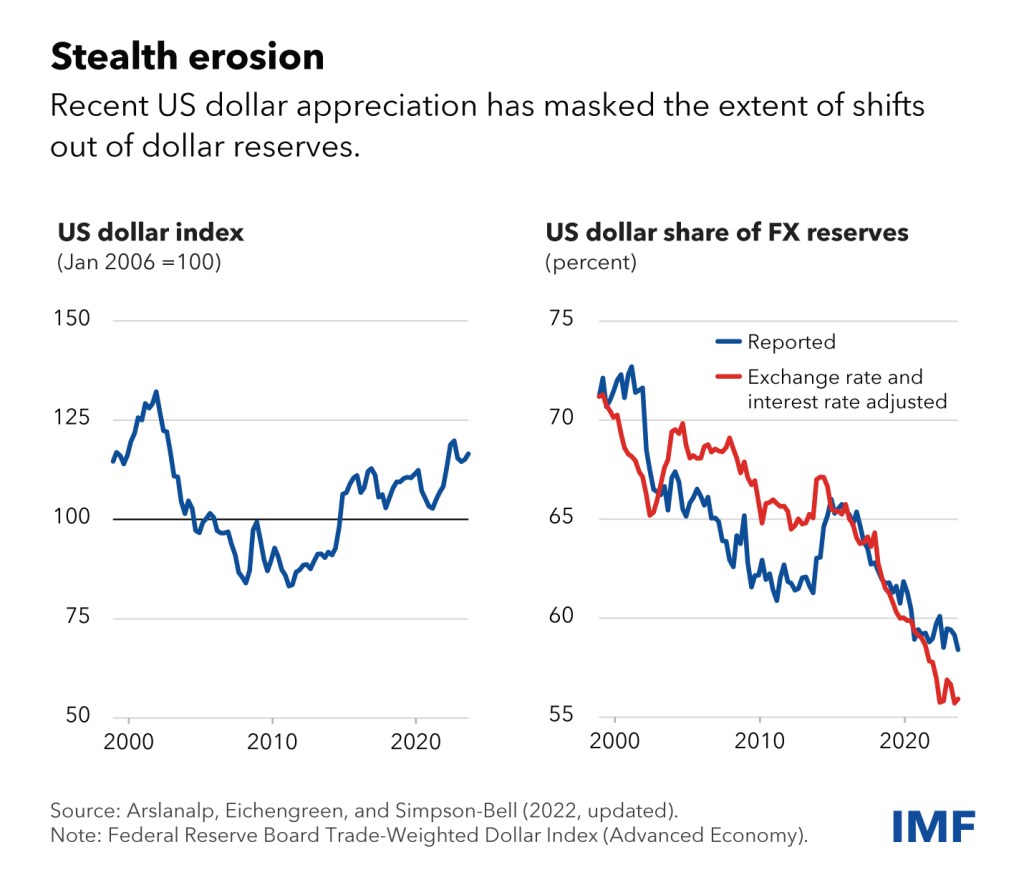

Multipolarity also implies currency diversification will become more important. Today, global central banks have already begun hoarding gold at an unprecedented rate and conflicting trends relating to the internationalisation of the Renminbi through Chinese carrot-and-stick diplomacy, as well as the growing use of digital currencies particularly amongst countries blocked from the SWIFT system provide incremental challenges to a Dollar-backed portfolio.

A world with no clear hegemon could be inherently less stable geopolitically (think of the pre-WW1 period), yet a stabiliser present today and absent amongst regimes prior is that today’s powers are deeply interconnected. Instead of large scale regional wars, we will continue to see an uptick in proxy wars, territorial disputes and a shift of direct conflicts to the cyber arena — all of which would create more frequent bouts of market volatility. The absence of the single hegemon also means global coordination on issues increasingly non-sovereign in nature become harder, such as climate change and trade rules. Investors (and members of the global community) today can no longer expect the global financial safety net to be adequate to fall back upon. In the defensive theatre, the lack of global cooperation and protectionism is also dangerous — neutral countries, with no security alliances or partnerships with others might be incentivised to take a page out of Charles de Gaulle’s book and build up their own nuclear programmes. This will walk us back on the nuclear non-proliferation, and threaten to create an unstable global corpus where nations and actors wield tremendous power to destroy.

On the flipside, multipolarity could boost growth by sparking competition and innovation across regions and blocs (we are seeing this in China, where they work to develop alternative and external fields of innovation especially in lithography). With blocs and regions vying for influence, there can be an impetus for countries to reduce exporting their savings to the US and investing in domestic capacity. This may drive productivity improvements and more critically new markets. For instance, the expansion of BRICS or ASEAN-led initiatives could unlock growth in previously marginalised economies. In Asia alone:

- It absorbed 30-54% of global FDI from 2019-2023

- Estimated 42% of global GDP will come from the region by 2040, with an estimated 55% of the global workforce

- Fixed investments are expected to increase to $140 trillion, surpassing the combined invesetment forecast for $89 trillion in the US and EU

- The region accounts for 75% of global AI patents by 2022

- Asia could account for 65% of the global middle class, with 700 million consumers added by 2030

Our view marries these points mentioned together: global growth might be slightly lower than in an integrated world, but multipolarity will also create new growth frontiers. We remain optimistic in the peripheries such as the Gulf nations, Southeast Asia and Sub-Saharan Africa, but remain cognisant the regime we are entering is one of elevated fiscal deficits and austerity-fatigue, which could also drive stronger nominal trend growth in developed economies.

The Erosion of Democratic Norms

For decades, the US has been upheld as the bastion of democracy and rule of law, which underpinned its economic strength and attractiveness to global investors. Recent developments going back to the Jan 6 insurrections, a disregard for judicial oversight and frequent calls to erode constitutional norms raise questions about institutional and societal resilience. As difficult as this topic might be, it warrants a frank analysis of the political and investment climate, central to long term risk assessments. Brookings published an article in late 2023, detailing a stadial decline in democracy in the US driven by executive overreach, politicisation of election administrations and entrenched partisan advantages via gerrymandering. More worryingly, the politicisation of the rule of law towards politicians creates a concerning outlook where no malfeasance can be kept in check.

Why this matters is because political stability and rule of law are foundational to a healthy and sustainable long term investment environment; we are rewarded during regimes of predictability, contracts that are enforced fairly (FTA deals are being disregarded today), regulations that do not suddenly become arbitrary, and sound governance. A study conducted in a States United Democracy Centre report succintly states “Democratic erosion weakens the rule of law, the reliability and impartiality of judicial authorities, and the provision of information” — all of which can increase risk for markets. In August 2023, Fitch Ratings downgraded US sovereign debt from AAA to AA+, citing an “erosion of governance”, specifically highlighting the events on Jan 6th as well as repeated political standoffs over the debt ceiling as symptoms of growing political dysfunction.

From our perspective, the rule of law in the US remains intact but highly vulnerable to further politicisation by machiavellian leaders like Trump. The US judiciary is still independent but is increasingly viewed as politicised alongside traditional media sources, who are no longer trusted to dispense reliable information by many Americans. More will turn to podcasts, interviews and content by at times unqualified and uneducated personnel, which further entrenches the crisis of misinformation. The whipsawing of regulatory requirements especially in environmental and energy regulations and antitrust enforcement philosophy is at times normal within a democracy, but the amplitude seems to have increased. Continued policy uncertainty will ultimately result in a reduction of investment and higher volatility.

Traditionally, investors have characterised the US as having negligible political risk and bestowing it the safe-haven status. Today, we have to apply the same political risk metrics we use elsewhere: institutional quality and resilience, political predictability, societal stability metrices … which the US still scores highly on most; but the margins of safety have shrunk. For instance, where we might have held overweight duration in the past during bouts of elevated uncertainty, we now consider neutral or underweight duration, prefering other safe assets including Gold and regional investment-grade credit as a small adjustment and not an overhaul.

From a long term growth perspectice, the erosion of democratic norms poses a clear negative if left unchecked. The US became the world’s most prosperous nation not just through a large population or plentiful resources but through institutions. Should those erode, we expect the entrepreneurial and investment climate will too. There’s already anecdotal reports of higher inquiries for second passports and offshore asset management by some with such concerns, though these could be pure diversification plays as much as it could be capital flight.

My job here is to consider tail risks, i.e. a scenario in which a disputed election leads to a constitutional crisis. How can we ensure portfolios withstand that shock? Most importantly, as active members of the global community, we should continuously espouse the importance of free and open dialogue, and the maintenance of the norms that have led to common prosperity and and uplifting of communities, societies all around the globe.

This is where we reiterate our commitment to developing geopolitical and political muscle within our decision-making teams. We continue to stay the path on US assets, believing in their potential in generating strong returns given the country’s immense strengths, but we are no longer willing to write off political risk as negligent.

Ultimately, an America that remains true to its democratic ideals and continues to lead the world is not just morally preferable, but economically and financially beneficial for the world. Hope aside, we will continually monitor the political situation in the US and adjust our positionings to better fit the increased range of outcomes.

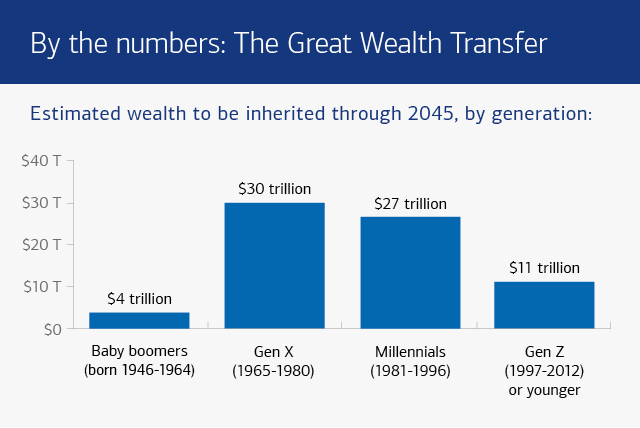

The Great Wealth Transfer

We are living in an epochal moment in the realm of wealth and capital markets underlined by the largest intergenerational wealth transfer in human history. In the US alone, an estimated $84 trillion will be passed down through 2045 and by 2048, approximately $124 trillion in wealth will have changed hands. In Europe, the average ultra-high-net-worth individual is near the 70s and the average heir is in the 40 – 50s age range.

The sizeable wealth transfer will have multifaceted implications for capital markets, consumption patterns and saving behaviours.

Changing Investor Profiles and Preferences

As wealth shifts to younger generations, the profile of an average investor will skew younger — resulting in a new set of preferences and risk appetites. Today, 75% of wealthy Millennial investors believe it is not possible to achieve above average returns through the traditional stock/bond portfolios and are looking for diversified return streams in alternative assets such as private equity, venture capital and cryptocurrencies. They also place higher emphasis on sustainable and impact investing to seek alignment with their social and environmental values. We expect increased flows into funds relating to these themes, as well as natural asset companies and green bonds that meet certain ethical criterias.

Portfolio Rebalancing and Market Impact

Wealth held by the older generations was concentrated heavily in blue-chip stocks, index funds, bonds and real estate, often accumulated through decades of conventional wisdom over portfolio construction. These portfolio allocations are likely to shift as we near the turn of the century, especially as younger investors look to divest traditional holdings for investing meaningfully.

We also see reasonable odds of a further shift in geographical allocation of wealth towards countries and regions with favourable tax regimes and political stability. Younger Americans and Europeans are much more likely to be globally minded and invest/migrate abroad as compared to parents who have become home-biased into domestic assets, and we prefer regions in Asia where social stability and predictable governance models lure foreign investors pose a refreshing picture relative to domestic markets.

Consumption and Saving Patterns

Recipients of the wealth transfer are poised to be individuals in their mid-fourties to early fifties, still often with the openness to make significant life expenses ahead (think repaying student loans, home-ownership). The transfer of wealth means millions of households and individuals today will become empowered to meet their obligations on previously deferred consumption, providing a boost to certain sectors including housing (homebuilders, insurers, banks), consumer durables (cars, appliances) and discretionary services (travel, dining). Within the strategic term, we see the potential for the middle-aged communities to move out of renting and becoming homeowners.

Looking forward, savings behaviours may also shift. Boomers currently hold significant assets in retirement schemes which are invested conservatively, whilst younger investors have a preference for moderately higher risk taking and enhanced sources of returns through illiquid alternatives. This phenomenon is not just behavioural but practical: many youths have less access to defined benefit pension schemes and will rely on their individual contributions for retirement. An increase in consumption behaviour and decline in conservative savings also potentially adds to structural inflation, and could be an important contributor to elevated rates for longer.

For investors and wealth managers, this moment is crucial in establishing relationships and reinforcing commitments to fiduciary standards. Estimates believe over 80% of wealth heirs are likely to change advisors after inheriting wealth, often because of a lack of relationship with their parents’ advisors or a preference for a different style. Being nimble and genuine will be key — understanding the different risk profiles and preferences means the implementation of digital tools such as robo-advisors, mobile banking platforms and incorporating sustainability efforts to appeal to younger clients. There could also be a further consolidation in the wealth industry as firms compete to scale and invest in technology to serve this coming monumental transfer of clients.

From a macro perspective, this wealth transfer could represent upside potential to productivity and growth if funds are deployed into new ventures and technologies. For example, a middle aged investor inheriting a manufacturing business is much likelier to invest heavily in AI and robotics competencies than an aged business owner, and likewise is likelier to invest in promising start-ups through venture capital funding.

In essence, the largest wealth transfer in human history will necessitate a restructuring of the opportunity set investors are familiar with. It is not a disruption but a beautiful reconfiguration towards leaving meaningful impacts on the world around us. As long term investors, we view this largely as an opportunity; new investors bring new ideas, energies and renewals. The financial industry will be forced to adapt and some asset price dislocations might occur as holdings change hands, but we are confident efficient capital allocation will continue.

To bridge the old and new is to be engaged with the inheritors and the financial landscape that will facilitate the wealth transfer. The change will influence what themes and sectors we invest in; how we invest, and who we are investing with.

Moreover, we have become concerned with the increasing state of wealth inquality in the US and other developed economies. The top 10% of wealthy Americans today hold 93% of stocks and 60% of the wealth, which means retail consumers and average households increasingly get crowded out of capital and spending. We expect consumer discretionaries like Walmart and Dollar General to serve less utility in forecasting the strength of the US in the future, as wealth becomes concentrated in the affluent classes that do not rely on these mass market grocers. In addition, consumer sentiment surveys are also likely to become less ideal of a predictor, since equity and capital owners are likely to not be the ones as affected by worsening sentiment on the ground. It is possible that this phenomenon has already occured, where consumers report tighter conditions and capital prices remain elevated due to the disconnect between the average consumer and capital owners.

Navigating the Decade Ahead

The themes we have explored here, from the risk of private markets to geopolitical realignment risk us appearing overly pessimistic about the global outlook. While we acknowledge the world has entered a period of flux and unconventional business cycles, this does not mean the opportunities we like have become out of reach. Investors today are required to be more agile, more informed and more forward-looking than ever, but we look forward to the challenge of finding opportunities amidst dispersions especially as previously un-investable markets become attractive.

Throughout the period of change, it is crucial for us to stay steadfast to our core principles. We will continually promote sound, long term strategies grounded in an interdisciplinary and diversified approach to tackle the Gray Rhinos and Black Swans proactively. Investing across assets and geographies, our task is to integrate insights into a cohesive strategy, which means staying involved on both sides of the risk spectrum by hedging against macro risks and leaning into transformative trends, and continuously revisiting our assumptions. Humility and adaptability will be key virtues looking forward, and we must be willing to change our minds and models alongside it.

The decade ahead will likely bring exciting surprises both positive and negative. We look forward to breakthroughs in major disease, deployable quantum computing and peaceful geopolitical resolutions that lift the world, but also stay prepared for shocks that test us. To be truly diversified means to craft portfolios that have different underlying return drivers, and that can be challenging especially when changes and risks today become foundational. This means that aside from the geopolitical dividend to be reaped today, there will be a premium attached to understanding systems, such as complex interconnected semiconductor supply chains or demographic shifts in Africa.

In closing, we reiterate our commitment to long term opportunities through diversification across themes and geographies, and a disciplined approach to risk management as well as a preference for forward-looking innovation.

Leave a comment