For the purposes of this article, a long-term triple sell-off refers not to net selling of US triple assets (dollars, stocks, bonds) but a slowdown/pullback in net buying of said assets; decade of compression refers to the belief the next 10 years will be characterised by weakened real equity market returns vis-à-vis the prior 10% annualised returns investors enjoyed, at approximately 3-4% in real terms.

There is a unique and innate challenge that faces the investor, who young in age, has not lived through the highs of the 80s high yield bond growth, troughs of the Dot Com bubble burst or the decimation invoked by the Great Financial Crisis (GFC). Instead, my horizon was formed in the aftermath earmarked by a regime of secular stagnation and cheap credit as corporations, businesses and investors alike rebuilt their balance sheets, so it does invoke some dissonance to be thinking of a rejection of assumptions regarding the growth expected off long-term compounding returns and the conventional Buffett wisdom.

There are numerous factors which influence by belief of an impending decade of compression marked by a triple sell-off (and these factors compound each other). The first is the recent implementation of the OBBBA, but more importantly the OBBBA as a representation of the US’ unwillingness to tackle the debt problem. It is one thing to parrot about the need of fiscal responsibility, but another entirely to pass a spending bill that is projected to widen the fiscal deficit by 5 trillion on a permanent implementation basis, poised to keep the nation running at around 7% annual deficits. Economists have estimated the effect of the spending bill will be felt the strongest by 2034, when the debt-to-GDP will have reached 129%, up from the current 98%; growth itself is projected by the Yale Budget Lab to slowdown by almost 3% by 2054 than if the fiscal and tax bill wasn’t passed.

And there is the proliferation of partisanship and political brinksmanship. The splitting of the overton in the US is not novel; the brightest of minds have been deliberating over the applicability of the median voter theory since the 90s, but today when more issues than ever before are split along party lines or across ideological spectrums, voters find themselves incapable of reconciling or making concessions to look for an optimal outcome. At the sovereign level, we start to notice necessary reforms are not able to be made no matter how critical they might be. What this means is the US may start to lose dynamism, stymied by political impasses and self-destructing scores going for cheap points rather than the best for the nation. From the business and investor’s perspective, the best value a country can provide is the business of certainty; the provision of policies, rules and laws that do not drastically change over the lifetime of a company’s planned investments. The current whipsawing in between further polarised camps on the political dyad further accentuates the US lack of ability to provide certainty internally but also in industrial, economic and trade policy. This raises questions not just on the end of sovereign and social fabric risk, but also on the reliability of the US to act as custodians and denominators of significant foreign reserves held in stocks, bonds and dollars.

In the coming decade, spending in the US will only continue to grow. In this strategic decade of competition, the country will have to spend more to invest in national security, be it in homegrown supply chains, new weaponry, or the Golden Dome. And immutable laws governing the world, such as the shifting demographics and ageing populations, the need to provide sustainable financing, or the build-up of AI related capabilities through investments in grid infrastructure, energy storage solutions or data centres will all require new and more financing.

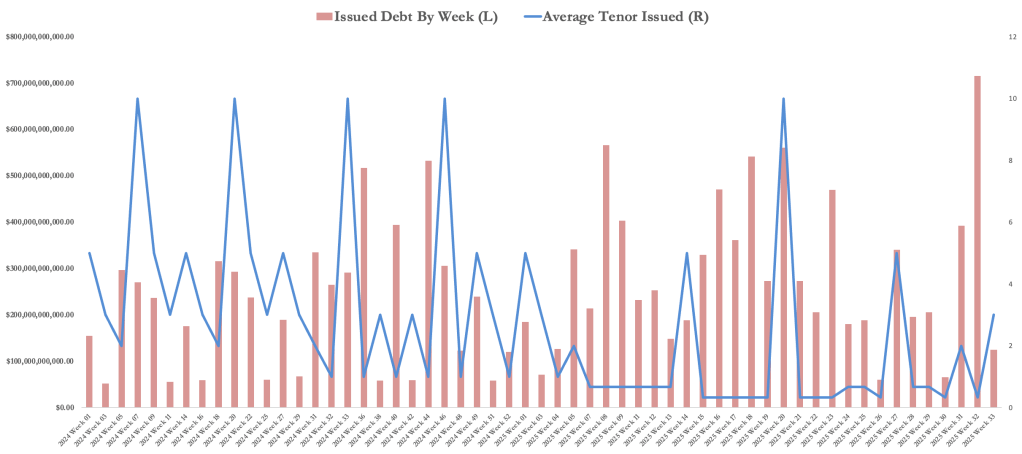

The cumulation of these factors weighing on the spending end of the fiscal issue means we are likely to see interest payments exceed total social welfare benefits in the near future. What this means is the US becomes less able to invest in communities, to democratise access to higher education across states which need it the most and continue to starve new innovative startups from securing crucial financing by relying on stopgap budget measures, which has left American ship makers and legacy industries entrenched in an acceptable status quo of mediocrity. Today, there are already around 4000 zombie firms in the US; 45 million working age adults are currently on a study loan and 24% are delinquent and in 2010, 50% of new home buyers were first-time buyers; today the number is 24%. The effects and signs of communities becoming malnourished and whole cities being underinvested in are already showing. And as our ability to reduce non-discretionary spending is stymied by an uptick in populist sentiment, budget impasse and growing spending needs, the US will continue to grow its debt issuance and at shorter tenors to avoid paying out rising term premiums. This means firms and businesses will start to experience greater crowding out in the credit markets, driving up borrowing costs and reducing available funding capacities for businesses and communities.

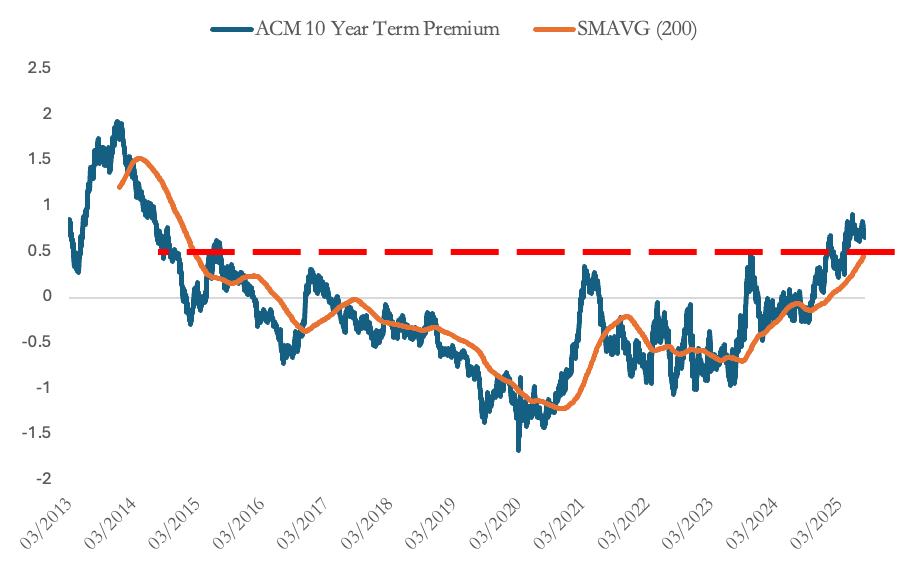

Term Premiums have reached the highest in 11 years

Source: Bloomberg

Loan Issuances have been growing, and at shorter tenors

Source: Bloomberg

Even while we continue to depress the spending end of the fiscal problem, the US remarkably also restricts its ability to encourage growth. Today, the administration dangles investment funding allocated for institutions of higher education as a carrot on a leash, as if universities unilaterally benefit from the research output they provide. The weaponisation of access of international students to the best universities in the country has also created a climate of fear and uncertainty not just for existing students but potential ones, who now are being asked to weigh choosing to cross the pacific for the privilege to pay ludicrously expensive tuition fees in a country that might not want them. Many industry leaders and senior executives have publicly talked about the importance of the H1B and keeping America open to the best talent internationally. And growth is already establishing itself as the consensus mechanism in which we decompose the US’ structural deficit; any headwinds to growth drastically reduces the ability to repay debts, finance new budgets and spendings, as well as forcing us to default on our obligations to the next generation.

At the same time, it is not just the knowledge-based economy of the US that is at risk from their restrictive immigration policies as well. Whilst controlled and regulated borders are undoubtedly essential to maintain the rule of law, the current administration’s actions have at instances crossed into fear and the use of threats, which run the risk of disincentivising legal immigration on the grounds of a climate of high-stakes unpredictability.

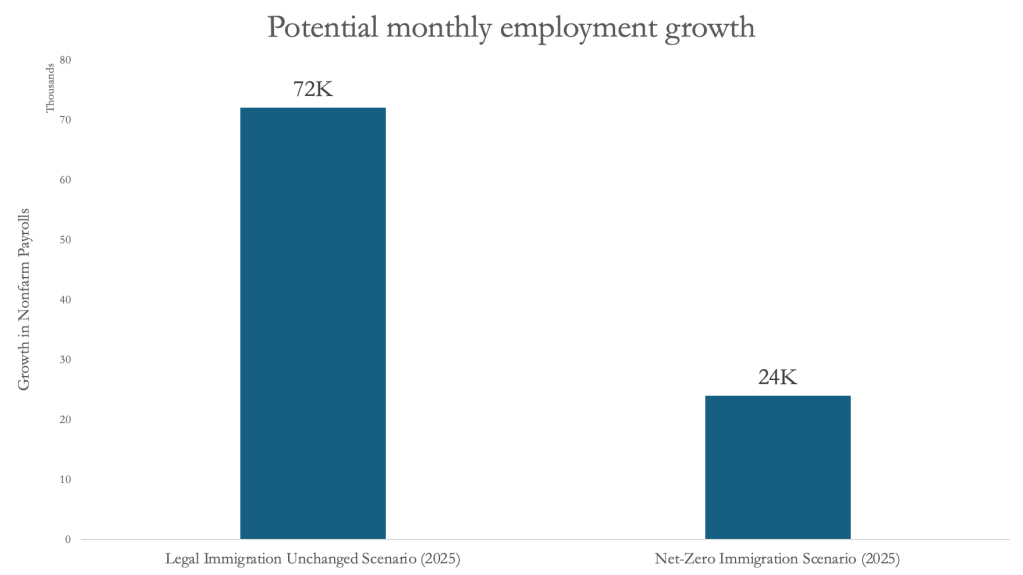

Recent data released from Apollo Global Management show that current estimates also have the US deporting about 3000 immigrants every day, putting the labour supply decline in 2025 at 1 million. The total number of southwest border encounters has declined to near zero this year, while 3.8 million immigrants in the country are on limited or “twilight” status, which themselves are being suspended or terminated. Unauthorised workers in the US today make up around 43% of work in crop and agriculture and are significant in the construction and hospitality sectors and provide an important source of low skilled labour in the US.

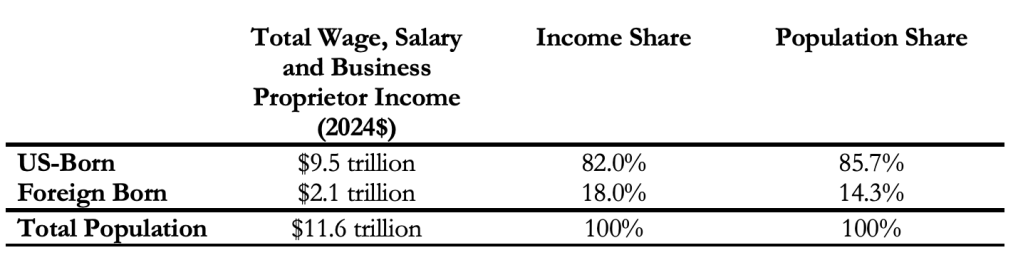

Immigrants Outsized Contributions to the US

Source: Economic Policy Institute

By engaging in employment, immigrants disproportionately benefit the economy because they tend to be in prime working ages and are more likely to start businesses. At the same time, they contribute significantly to economic growth and growing the size of the labour force; the benefit of immigrant participation in the US economy in 2022 was measured at $1.6 trillion in added economic activity and over $579 billion in local, state and federal taxes, according to the Council of Foreign Relations. At the same time, immigrants also face inhibitive restrictions on access to social welfare programs funded by the Federal government, such as Medicaid, food stamps and the Supplementary Security Income scheme. All in all, a cumulative deportation of over 1.3 million immigrants, who contribute immensely to the nation’s economic growth, talent development and taxes paid whilst receiving minimal Federal assistance, would increase inflation sizeably due to the tightening labour market conditions and contracts the real GDP and employment statistics.

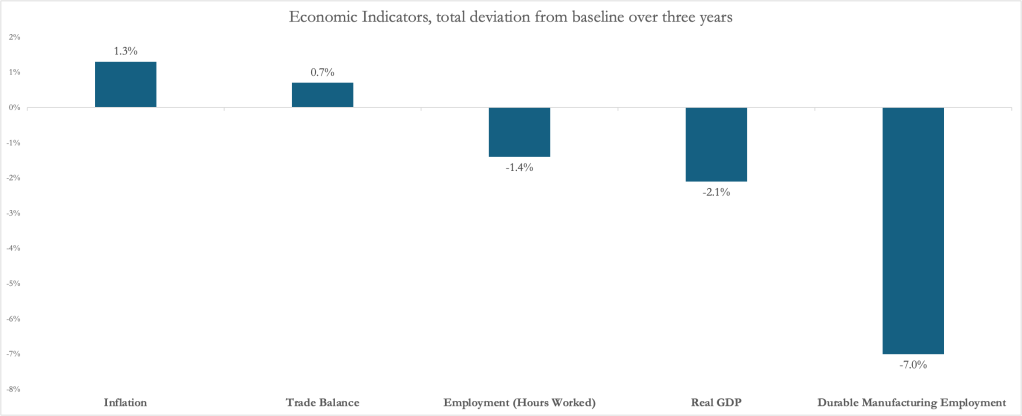

Strong immigration policy play-out scenario

Source: Apollo Global Management

Source: Apollo Global Management

I also worry over the potential characterisation of DOGE-led initiatives, which run the risk of having any proposals to keep government leaner and more effective being shut-down immediately and labelled Trump or Elon esque. Reforms to the bureaucratic inefficiencies are absolutely needed almost everywhere around the world and much less in the US where cybersecurity, treasury and other administrative infrastructures are old and outdated, and I fear all future steps taken by subsequent administrations to keep the state apparatus efficient will meet severe accusations of overreach.

And finally, the US alienation and hostile actions taken towards its allies indiscriminately, where friends and foes are simultaneously slapped with trade actions add the cherry on top, where institutional investors around the globe now are more conscious of where their currency exposures are and are forced to actively hedge their dollar exposures. The model of creditor nations, largely prevalent in the Asian countries, is now much less feasible as countries look towards regionalisation of trade and lower structural exports to the US.

In response to the above headwinds that make likely the decade of compression, the US might decide to take on two alternative sets of decisions.

If the US chooses not to Japanify by inflating their debt away and punishing bond holders through a rampant credit creation cycle, concerns over fiscal sustainability trends will not immediately drive global investors away from dollar-denominated assets, but the rate of decline of marginal purchases of dollar assets will grow in haste because no investor on the planet is aware of when exactly the camel’s back is broken. We will see currency diversification trends into countries with embedded fiscal premiums, such as in Germany and Korea (with their strong current account surpluses trend), or dollar assets become much heavier hedged than in recent memory, providing headwinds to returns repatriated back to domestic currency terms. As global investors slow down the rate of marginal purchases of US treasuries and think twice about dollar exposures, term premiums reach new highs (the ACM is already at 0.8) and investors demand higher compensations for taking on added sovereign and fiscal risk. Yields continue to grow and interest payments continue to dominate fiscal spending.

In addition to interest payment dominance in spending plans, the increased need to finance spending through raising debt further crowds out private investable bonds in the public markets. Corporate loan issuances struggle to find access to credit as government institutes practices that reward the ownership of sovereign over private debt, while the Treasury struggles likewise with a retreat of foreign central bank purchases of issuances. Essentially as the demand weighs on the treasury market, enterprises and corporations will begin to find not just the cost of credit expensive and inhibitive, but also a government becoming dominant in the credit market. In this scenario, the dollar weakens and firms with sizeable balance sheets struggle with heavy book losses. Rates rise faster, and discounts on equity valuations becomes greater, leading to the decade of compression.

On the flip end, to deal with increased fiscal impulse and the need to expand credit access, the US can embark on a similar post-GFC route with rampant credit creation, but this time instead of rebuilding corporate balance sheets, the aim will be to repair sovereign balance sheets and inflate off debt. This scenario has a likelier probability because the inflation-tax to meet debt obligations are much more politically feasible relative to the imposing of punitive taxes on individuals and business. By expanding the rate and scale of credit creation, the government drastically expands the monetary supply to meet conflicting needs in the economy and winds up the central bank holdings of treasury instruments. Today, the Federal Reserve owns approximately 40% of all outstanding treasuries, and I expect the number to become much larger if quantitative easing at scale is undertaken. It is also crucial to note once such action is taken, it becomes incredibly difficult to reverse the extensive distortions to the treasury market that the central bank would have done by owning equal or more than half of all outstanding debt.

Ceteris paribus, the rate of rampant credit creation and net portfolio purchases driven by domestic absorbers of US debt and assets potentially drives the dollar weaker, especially if investors continue to look for global investable alternatives as they have done in the first half of the year; think European investors, who in EUR terms have seen miniscule returns from the US equity markets relative to the missed rallies from domestic capital markets. While large-scale central bank buying at the long end of the curve (but the US has demonstrated a preference for shorter-dated issuance recently to retain optionality and agility, as well as expectations for a dovish Fed Chair in a year’s time) will drive down rates and keep bonds strong, we have been noticing, and I posit, that worries about fiscal path and the sustainability of US debt acts as a strong counteracting balance to the headwinds for bond owners, especially with strong supply-side dynamics of the treasury market. Net, the path outcome of rates may be lower, and bonds might be marginally stronger, but I expect an acceleration in the weakening of dollar fundamentals, trimming foreign currency denominated returns for portfolios around the world.

The commonalities for US asset holders in both scenarios are clear and remarkable. Foreign investors, faced with a more uncertain US outlook plagued by political rife and fiscal concerns will pull back duration of dollar assets and potentially overweight short-term holdings, with a preference for active and dynamic portfolio management especially amongst global pension and sovereign wealth funds. Investors globally undergo a mentality shift away from one of active holdings and partnerships/investments with strong and promising businesses, to one of a no strings attached, pure tactical opportunistic framework. As a result, strong companies with robust fundamentals but lack growth and tantalising short-medium term industry catalysts lose attractiveness to the growth and compounding investments that can generate a ROE in strong excess to the heightened rate of discount arising from fiscal, political and global headwinds. And crucially, once actions that seek to undermine your friends and allies are taken, trust is not easily repaired. Today, the EU is actively seeking FTAs and closer links with the world ex-US, such as their increased reaches to Mercosur, China, and a long-awaited realisation of the need to build strategic autonomy. These measures taken deliberately by the US to create an America-Alone path should not be mistaken to be transitory and administration dependent; look no further than to the Biden Administration’s difficulty in winding down Trump 1.0’s tariffs (or perhaps trade policy has become bipartisan, which also works to reinforce the point made). As the former Prime Minister of Singapore recently put it, by the next US elections in 2028, there is no politically feasible way to have domestic industries protected and insulated through strong tariffs for the past 3 years, and then campaigning to upheave the livelihood and profitability of these local businesses and firms by removing these protectionist measures. So I do believe the strength of Pax Americana accrued through the diffusion of American economic and corporate strength abroad, such as during the Marshall Plan, will face a decade characterised by unique geoeconomic headwinds.

The “American risks” embedded in the minds of global investors are clear and tangible. The use of sanctions, dollar-funding threats and unilateral actions made by the US has sparked a gradual rise in global demand for non-dollar denominated transactions and invoicing and for some, the push to proliferate bloc-currencies (which faces a whole other set of challenges on its own). Though the likelihood of the emergence of an alternative reserve currency within the next decade as per our contention is unlikely because of the treasuries’ unrivalled status, there is no doubt countries are beginning to concern if they want to continue exporting dollars to the US, holding significant reserves in US dollars and maintaining a hefty reliance on the fortunes and whims of the US, an increasingly unpredictable and unreliable ally. Just this April, Germany announced its consideration to withdraw its 1200-ton gold holdings from the Federal Reserve due to concerns about the safety and reliability of the US as a custodian, particularly under the current political climate and policies of Trump. The unwillingness of global asset holders to keep financing treasuries, managing their dollar exposures coupled with the growing opportunity set to direct one’s investments outside of the US will create a reinforcing loop, where uncertainty over path of US and dollars + reduced willingness to invest in the US + a pullback of duration + expectations of stronger-than-before depreciation will result in an unavoidable winding down of American exceptionalism. And while the European region remains underinvested and de-industrialised, I do not see a credible reason for the region, who is interested in building up an integrated capital markets union and facing unprecedented threats and hostility from Washington, to continue exporting the equivalent of EUR 3 trillion each year to invest in America, keeping their businesses well-funded and liquid whilst intra-regional firms in Europe express malaise over the difficulty to raise funds at the scale the US does.

The result of such will lead to the materialisation of the decade of compression narrative, where equity market returns are compressed relative to historical averages. Selective flows into growth and strong thematic investments such as the AI-buildout for excess ROE further the indexation of the S&P, starving off investors with alpha-generation opportunities and sending them abroad to invest in markets with stronger dispersions. The greater discount on equity returns leads to an annualised 4-5% of real returns and less on a currency unhedged basis. Dispersions between large corporations and smaller businesses grow as headwinds such as inflation, weakened employee leverage (due to the effects of AI on career mobility and employment) disproportionately impact smaller enterprise and benefit larger institutions, which are endowed with the balance sheet sizes to adopt revolutionary technologies at scale and weather through the higher-for-longer period of inflationary pressures. Together, the business landscape in the US might continue to struggle from a further pullback in investment (in real dollar terms) into communities and human capital development, leaving students with a higher incidence of lower credit scores and businesses with an uptick in default rates.

The compressed equity market returns become troubling because of the immense wealth effect felt by the American public. The average American household today holds approximately 40% of their household wealth in equities, far in excess compared to their global counterparts. Whilst the proportion is small relative to the 70% of Chinese household wealth in real estate, the effects on the US’ consumption based, capitalist economy could be as great gradually.

US-listed companies usually trade at a 40% – 70% valuation premiums over global peers because of the dynamism of the country and its private sector, its unique ability to take innovation from zero to one but most importantly the trust global investors have in the system ushered by the US. A breakdown in this critical trust, as evidenced by the comments made publicly by Merz and Bayrou this year, serves to compress the spread on fair value investors are willing to pay and accept for US-stamped assets. And when investors are no longer willing to pay and accept a valuation premium as high in the US, there will be more incentive to align as well on the profitability and value end, with greater regionalisation trends, where firms may choose to list in domestic and regional stock markets for convenience and proximity.

Today China’s vast industrial and state-directed investments over decades have paid dividends, whilst the US seeks to take its anti-China step too far and do precisely the opposite. China now vastly outranks the US in cumulative and publication rate of highly cited papers in AI technologies, Machine Learning and Adversarial AI; all key areas labelled as National Security concerns by the US government. Whilst the US remains the critical hub where they can take innovation from zero to one, China’s advancements in their target theatres of the Made in China 2025 decade-long project demonstrate the advantages and effectiveness of targeted state-directed policies over flip-flopping regimes in the West, where the UK has had three Prime Ministers in as many years and the US seems unable to find commonalities across the spectrum.

There are a couple of possible factors that could lead to the world in a decade’s time turning out rather different from this initial visualisation.

The first is critically the availability of alternatives with regards to sources of returns in global capital markets. The US today still boasts the world’s most dynamic, deep and robust capital markets; unicorns from around the world still choose to list in the US, buoyed by its strong fundraising environment and deep pool of entrepreneurial and technical expertise. Importantly, as investors and pensions find increased obligations to be made to the generation before us, they find no alternative but to look for sources of highest returns to be able to meet those growing obligations. Pensions are already starting to explore the field of private assets, and I do believe if corporate reforms and structural changes to capital markets globally do not take off as strongly as hoped (Japan continues to face structural headwinds in terms of mindsets, for example); investors who need and want to generate the best returns per unit of risk will continue to be forced to stay exposed to the US markets. In this scenario, the lack of alternatives in global equity markets keeps investors resigned to staying invested within the US, keeping global portfolio participation of US assets stable or growing, as investors look towards higher return generation markets entirely.

The other side of the coin details a world with equity market dispersions. Countries like the UK, Canada, Korea, Japan among others potentially successfully enact shareholder reforms, and the European Union potentially lowers trade and investment borders within. Global investors enjoy the optionality to deploy capital in Developed Markets ex-US and are rewarded with competitive longer-term returns. And at the same time, due to structural demographic trends, developed economies such as Japan, the United Kingdom and eventually the United States will lose capital market and economic competitiveness as the dynamism and capitalist tendencies become eroded in favour of democratic socialist measures. Think in terms of societies, with a larger propensity of older workers. Governments become restrained from allowing capitalist and laissez faire principles to run, moving in favour of frequent and automatic stabilisers on the risk any increase in unemployment to the labour force becomes structural. The contrasting image is Emerging Markets, with much favourable demographic conditions and are able to tolerate more short term market dislocations and periodic unemployment to promote efficient usage and distribution of capital. This means we could potentially see a world where Emerging Markets provide not just more dispersions and a wider opportunity set for alpha investors, but also stronger compounded returns over time as businesses, firms and the economy is kept competitive without comfortable sovereign backstops during cyclical downturns.

In this scenario, deregulation and the AI build-out become more critical as the US looks towards maintaining their role as the leading edge for capital market activity. From both deregulation and AI growth, the US must cumulatively unlock more private capital than financial outflows/slowdowns in net inflows arising from portfolio diversification trends; while the global expenditures necessary on transformative changes grows, which reduces the size of surpluses to invest in dollar assets, and also regionalisation, which can compress the volume of recycled excess savings into the US. At the same time, AI growth must begin to deliver tangible ROI benefits and spur widespread growth in productivities and output to be able to generate relative returns in a world characterised by a higher equity discount.

An overt focus especially within the West about being politically correct also poses headwinds to long-term growth trends. Already, universities such as Harvard and Columbia are bringing up observations that their campuses are not encouraging or conducive of a diversity of ideas and opinions. I strongly believe political correctness stifles necessary conversation and discourse in critical areas particularly because political correctness represents a form of silent censorship. The key areas that need the most genuine talk are generally terrorism and immigration. And political correctness is at the core, fundamentally a data obfuscator. If information and data today is parsed through a layer of checks for political correctness, there will be a critical layer of data loss because even politically incorrect information convey truths, such as what people on the ground might be thinking about certain policies and developments in their neighbourhoods. Losing such data affects the efficacy and ability in the systems and AI algorithms to interpret and decipher the world around us, and we will find the benefits of AI more nuanced when the proportionate quality of data inputs decline.

At the same time, many factors which led to American strength still hold. To quote an article published recently on the Financial Times, even amidst the global uncertainty and tumultuous period we have been in, the US economy has gradually became incredibly shock-resilient, which keeps equity valuations attractive. Household debt to net worth is at all-time lows; households have half their $129 trillion of financial assets in instruments yielding upwards of 4% per annum, and corporate profit margins sit at 13.8%. The best and brightest still overwhelmingly choose to enrol in American universities; the most promising startups around the world still hold faith in the vibrancy and financing capabilities of the American capital markets and the private sector of the US still invests at a scale unrivalled in any other part of the world. So, there could very well be a world where the US continues to stay exceptional despite the vast array of case-specific headwinds to its innovation and status as a bastion of freedom and opportunity.

The dilemma now lies in if we choose to selectively invest thematically, or position dynamically and prioritising staying agile.

Recent developments and rapid re-ratings of longer-term asset investments means we can be punished not just on the time value of money but also the repricing of opportunity, which means the era of investing in compounding value is over and we demand investable opportunities in growth where short and quicker compounding delivers ROE sufficiently in excess of discount factors. Investors would be well positioned to consider allocations to private market opportunities carefully, where exposures provide attractive return per unit of risk relative to over-indexed equity markets but come with their period of 30-90 days of illiquidity. And at the same time, would it be truly a de-risking to diversify across sectors and industries in developed markets? Just as the fibre cables, internet developments of the 1990s pulled mass investment and funding away from manufacturing and other sectors, data centres and AI remain the overwhelmingly favoured investment avenue today. ROE argument aside, the risks of a sector agnostic, thematic portfolio that investors run around the world risks investing in sectors struggling to find funding relative to the AI build-out.

We look at global changes and find anchors in immutable laws, one such being how fast firms and countries can re-route Ricardian efficient supply chains, or reciprocity in foreign relations. One tailwind here might be that thematic investments, that seek to capitalise on the immutable trends and directions of the world, such as investing in paediatric care, grid infrastructures, the future of finance… will provide the resilience to portfolios. And on the flip side, it is not just the extent of macro shocks that have increased dramatically over the last few years but also the speed of which these macro shocks come into play. Perhaps even thematic investments, which themselves seemingly provide investors with laws of the world to invest in, might not provide the speed and dynamism in which investors of the future must have.

Leave a comment